You are a responsible driver. You have a perfect record, you’ve paid off your home, and you’ve carefully managed your retirement savings to ensure you never become a burden to your children. You carry car insurance because it’s the law, and you likely assume that being “fully insured” means you are fully protected.

But here is the sageWISE Warning: If you are carrying “State Minimum” liability limits, you are effectively self-insuring your retirement against every irresponsible driver on the road.

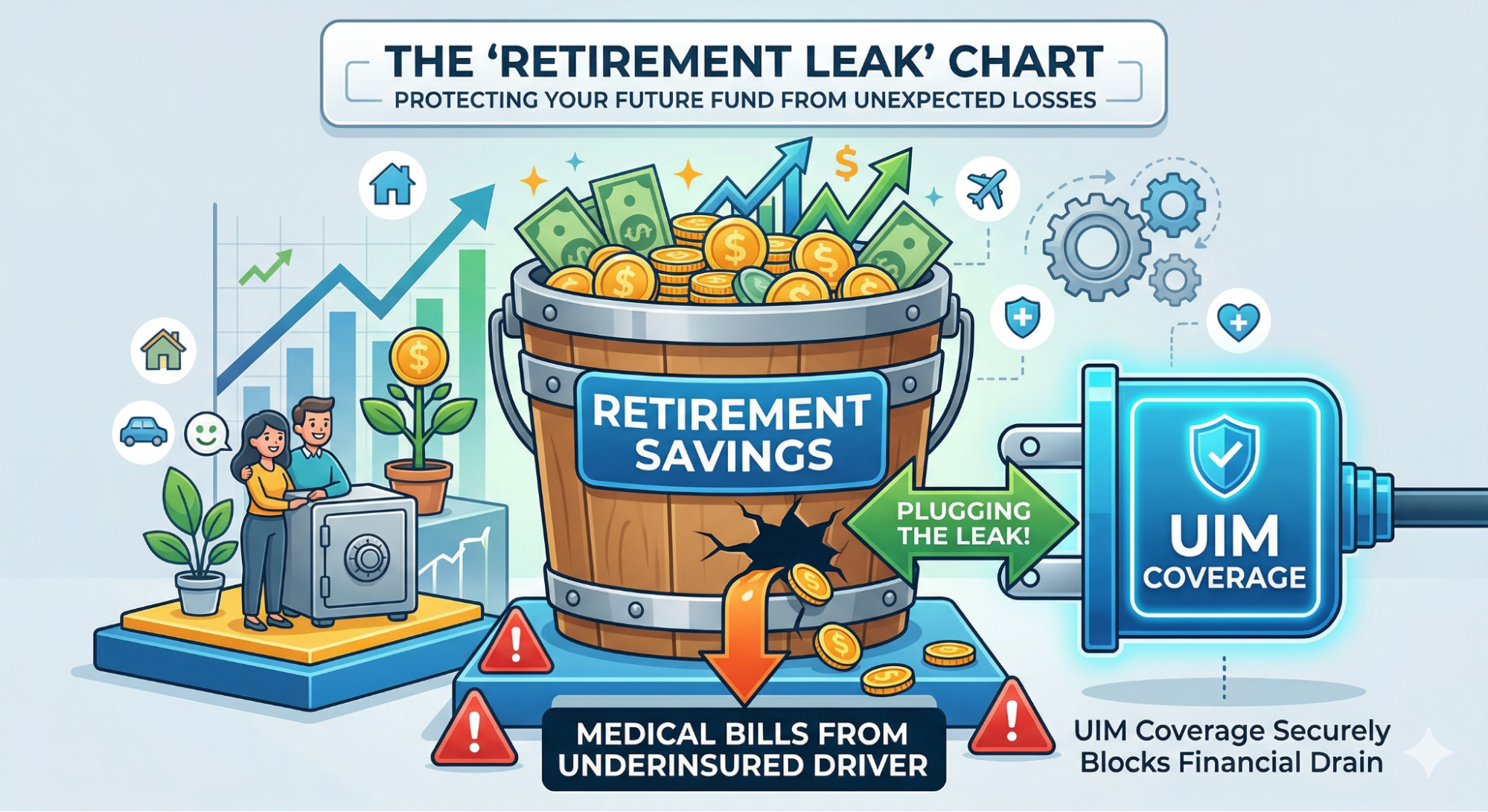

In 2026, the cost of a single night in a trauma center can exceed $15,000. If you are hit by one of the 30 million uninsured drivers in America, or a driver with only “basic” coverage, your “State Minimum” policy will leave you with a massive funding gap. Without a robust Uninsured/Underinsured Motorist (UM/UIM) Shield, a single red-light runner can drain your Annuity income, force a Reverse Mortgage to pay medical bills, or even put your home at risk of a judgment lien.

As your trusted advocate, we have performed a Sagewise Audit of the 2026 uninsured motorist landscape. We will show you the math of the “Minimum Trap,” explain the difference between UM and UIM, and help you calculate the exact “Asset Protection” limits you need to keep your nest egg safe.

Key Takeaways

- The “Minimum” is a Floor, Not a Ceiling: State-mandated limits (like 25/50) are designed to protect the public, not your retirement.

- The UM/UIM Shield: This coverage pays you if the other driver has no insurance or not enough insurance to cover your medical bills.

- The “Stacking” Multiplier: Learn if your state allows you to multiply your coverage based on the number of cars you own.

- The sageWISE Tip: Your UM/UIM limits should always match your Bodily Injury Liability limits. If you have $250k in protection for others, you deserve $250k in protection for yourself.

Stop gambling with your retirement savings. Audit your limits and claim your senior discount today.

Check Your New Senior Rate Now

The sageWISE Audit: The "State Minimum" Mirage

Every state (except New Hampshire) requires a minimum amount of liability insurance. For decades, many seniors have opted for these “Basic” plans to save $30 a month on their premiums.

The Trap: In states like California or Florida, the bodily injury minimums are often as low as $15,000 to $25,000 per person.

- The Medical Reality: According to data from the National Safety Council (NSC), the average cost of an evidential injury in a motor vehicle crash is now over $40,000. If the injury is disabling, that cost jumps to $155,000.

- The Math of the Gap: If you are hit by a driver with a $25,000 state minimum policy, but your surgery and rehab cost $125,000, there is a **$100,000 gap**.

- The Asset Risk: If you don’t have enough Underinsured Motorist (UIM) coverage, the only way to pay that $100,000 is to tap into your home equity or sell your investments. You are essentially paying for the other driver’s lack of responsibility with your life’s work.

UM vs. UIM: Knowing Your Two Defensive Shields

Seniors often see “UM/UIM” lumped together on their bill, but they are two distinct financial bodyguard protocols.

1. Uninsured Motorist (UM)

This kicks in when the at-fault driver has zero insurance or if you are the victim of a hit-and-run. Since nearly 1 in 7 drivers on the road is uninsured, this is a high-probability risk. UM covers your medical bills, lost wages (if you are still working), and pain and suffering.

2. Underinsured Motorist (UIM)

This is more complex. It triggers when the other driver has insurance, but their “per person” limit is lower than the cost of your injuries.

- Example: The other driver has $50k. Your bill is $150k. Your UIM policy covers the $100k “excess” so you don’t have to sue a driver who likely has no assets anyway.

The Math of Asset Protection: Why Your "Nest Egg" Dictates Your Limits

A 20-year-old with no savings can get away with state minimums because they have nothing for a lawyer to take. A senior with a paid-off home and a $500,000 401(k) is a “Target.”

The Sagewise Rule of Limits: Your insurance limits should reflect your Net Worth, not the value of your car.

|

Total Assets

|

Recommended UM/UIM Limit

|

Bodyguard Rationale

|

|---|---|---|

|

Under $100k

|

$100,000 / $300,000

|

Covers most non-surgical hospital stays.

|

|

**$100k - $500k**

|

$250,000 / $500,000

|

Protects equity and mid-sized IRAs.

|

|

Over $500k

|

$500,000 + Umbrella

|

Prevents total estate depletion in catastrophic crashes.

|

Financial Bodyguard Tip: Use our Car Insurance Rate Estimator to see the price difference between $25k and $250k in coverage. For most safe senior drivers, increasing your protection by 1,000% often costs less than **$15 per month**. It is the cheapest “Inheritance Insurance” you can buy.

The "Stacking" Secret: How to Multiply Your Protection

If you live in a “Stacking” state (like Pennsylvania, Florida, or South Carolina), you have a secret weapon to increase your shield without a massive price hike.

- How it Works: If you have two cars on your policy, each with $100,000 in UM/UIM coverage, “Stacking” allows you to combine them into **$200,000** of protection if you are in an accident.

- The Strategy: Always check “Yes” for stacking if it’s available. It provides a massive amount of “Phantom Coverage” for a tiny administrative fee. According to the Insurance Information Institute (III), stacking is the most efficient way for multi-vehicle households to secure their assets.

Step-by-Step: How to Audit Your UM/UIM Shield

Don’t wait for a crash to find out you are underinsured. Follow this roadmap today:

Step 1: Check your "Declarations Page"

Look for the abbreviations “UMBI” or “UIM.” If the numbers are 25/50 or 15/30, you are in the “Danger Zone.”

Step 2: Compare to your "BI" Limits

Most insurers won’t let you carry higher UM/UIM limits than your Bodily Injury (BI) limits. If you want better protection for yourself, you must also increase your protection for others. This ensures you are a responsible member of the community while shielding your own family.

Step 3: Inquire about "UIM-Conversion" (State Specific)

In some states, you can choose between “Standard UIM” and “UIM-Conversion.” Conversion coverage is superior because it adds the other driver’s limit on top of yours, rather than just filling the gap.

Frequently Asked Questions (FAQ)

No. As we detailed in our guide Does Medicare Cover Car Accident Injuries?, Medicare is a “Secondary Payer.” They may pay your bills, but they will also place a Lien on any settlement you receive. UM/UIM pays for “Non-Economic” damages like pain, suffering, and loss of quality of life—things Medicare never covers.

In most states, yes, provided there was actual physical contact between the vehicles. Some states have “Phantom Vehicle” rules that require a witness if there was no contact. Always file a police report within 24 hours to preserve your UM claim.

This is a huge senior benefit. Your car’s UM/UIM policy follows YOU, not just your car. If you are hit by an uninsured driver while walking the dog or riding a bike, your auto insurance shield will pay your medical bills and damages.

Agents often lead with the lowest price to “win the sale” or because they assume seniors only care about the monthly bill. As your financial advocate, we warn you that a “cheap” policy is a liability for anyone with a house and a savings account.

Surprisingly little. For most safe senior drivers, the jump from a $25k limit to a $250k limit is usually between **$80 and $150 per year**. It is the highest-value upgrade in the entire insurance industry.

Check Your New Senior Rate Now (Protect your nest egg. Secure your UM/UIM shield today.)