It happens in a heartbeat. You misjudge the distance to a concrete pillar in a parking garage, or someone taps your bumper while you’re in the pharmacy. The damage is minor—perhaps a $900 scratch or a cracked taillight. Your first instinct, honed over decades of being “fully insured,” is to pick up the phone and call your insurance agent. After all, that’s what you pay those premiums for, right?

But here is the sageWISE Warning: For a senior on a fixed income, filing a small claim is often the most expensive way to fix your car.

In the modern insurance industry, a claim isn’t just a payout; it’s a “Risk Trigger.” Even if the repair costs the insurance company only $500 above your deductible, that single entry on your CLUE Report (Comprehensive Loss Underwriting Exchange) can trigger a “Surcharge” that lasts for three to five years. By the time the dust settles, you may have paid the insurance company back three times the cost of the original repair in the form of higher premiums.

As your trusted advocate, we have performed a Sagewise Audit of the “Claim vs. Cash” dilemma. We will show you the math of the 3-year rate hike, explain the $1,000 threshold, and help you decide when to keep the insurance company out of your business to protect your retirement budget.

Key Takeaways

- The $1,000 Rule: As a general rule, if the repair cost is less than $1,000 above your deductible, you should almost always pay cash.

- The Surcharge Clock: Most insurers hike rates for 36 months following an at-fault claim, often increasing your premium by 20% to 40%.

- The “Zero-Dollar” Claim: Even “Inquiry-only” calls where no money is paid can sometimes be flagged on your record, affecting your Loyalty Tax status.

- The sageWISE Tip: Get a “Cash-Price” estimate from a local body shop before you notify your insurer. Once a claim is opened, it cannot be “erased.”

Stop the rate hikes before they start. See if you are overpaying for your current coverage today.

Check Your New Senior Rate Now

The sageWISE Audit: The Math of the "Surcharge Spike"

To be your own financial bodyguard, you must understand that insurance companies are not charities. They use a mathematical process called “Experience Rating” to ensure they never lose money on a small claim.

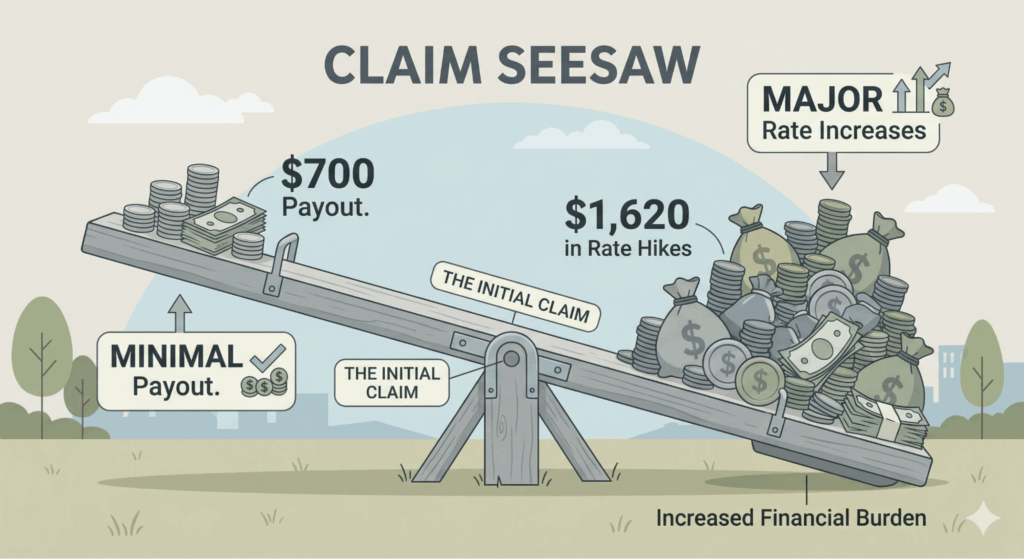

Scenario: A Senior with a $500 Deductible and a $1,200 Repair.

You have a minor accident. You decide to file a claim. The insurance company pays the $700 difference ($1,200 total – $500 deductible). You feel like you “won” $700.

The Reality Audit:

|

Year

|

Premium Without Claim

|

Premium With Claim (+30%)

|

Annual Loss

|

|---|---|---|---|

|

Year 1

|

$1,800

|

$2,340

|

$540

|

|

Year 2

|

$1,800

|

$2,340

|

$540

|

|

Year 3

|

$1,800

|

$2,340

|

$540

|

|

TOTALS

|

**$5,400**

|

$7,020

|

$1,620

|

The Verdict: By accepting a $700 check from the insurance company, you just agreed to pay them **$1,620** over the next three years. You “bought” a repair for more than double its market price. This is money that could have gone toward your Gold IRA or a family vacation.

The 3 Factors That Determine Your "Surcharge Risk"

Not all claims result in the same penalty. Before you decide, audit these three risk factors.

1. Your "State Threshold" Laws

Some states have consumer protection laws that prevent insurers from raising rates for small claims. For example, in some jurisdictions, insurers cannot surcharge you for an at-fault accident if the payout is under $500 or $1,000.

- Action: Check your state’s Department of Insurance website. If you live in a “Protective State,” the risk of a rate hike is lower.

2. Your "Accident Forgiveness" Status

Many seniors pay extra for “Accident Forgiveness.” As we noted in our Full Coverage Audit, this can be a valuable shield.

- The Trap: Accident Forgiveness usually only works once every 3-5 years. If you use it for a tiny $800 scratch, you are “unarmed” if you have a major $10,000 accident next year. Save your forgiveness for the big hits.

3. The "CLUE" Report Legacy

Every time you even ask about a claim, it may be recorded in the Comprehensive Loss Underwriting Exchange (CLUE) database.

- Why it Matters: If you try to switch to an Independent Broker next year to save money, the new company will see that “Minor Incident” on your CLUE report and charge you a higher “New Customer” rate.

When You SHOULD File a Claim (The "Must-Call" List)

We are honest brokers, and there are three specific “Financial Bodyguard” scenarios where you should ignore the rate hike and file the claim immediately.

- Multiple Vehicle Involvement: If you hit someone else’s car, you must file a claim. Even if the damage looks minor, the other driver could claim “whiplash” or hidden structural damage six months from now. You need your insurance company’s legal team to act as your shield.

- Injury of Any Kind: If anyone (including yourself) is hurt, refer to our Medicare vs. Auto Insurance guide. The medical coordination is too complex to handle with cash.

- Total Loss or Major Damage: If the repair exceeds $3,000 or the car is totaled, the “Surcharge Math” finally works in your favor. Pay the deductible and let the insurer take the hit.

Step-by-Step: How to Audit a Minor Accident

Don’t panic and call your agent from the scene. Follow this roadmap instead.

Step 1: Document for Defense

Take clear photos of both cars and the surrounding area. If the other person says “don’t worry about it,” get that in writing via text if possible. You need a record in case they change their mind later.

Step 2: Use the "Rate Reality Check" Tool

Before you guess at the cost, see what your car is worth. If the car is only worth $4,000, a $1,500 repair is a “Total Loss” scenario. Use our Car Insurance Rate Estimator to see how a claim would affect your specific profile.

Step 3: Get a "Private" Estimate

Go to a reputable local body shop. Tell them: “I am paying cash and not involving insurance. Give me your best ‘out-of-pocket’ price.” You will be surprised how often a $1,500 “Insurance Quote” becomes a $900 “Cash Quote” because the shop doesn’t have to deal with the insurance company’s paperwork.

Step 4: Check Your "Discount Shield"

Use the Senior Driver Discount Finder to see if you have any “Safe Driver” credits active. Filing a claim will strip these away immediately, adding even more to your 3-year cost.

Decision Checklist: Claim vs. Cash

|

If this is true...

|

Choose...

|

|---|---|

|

Damage is to your car only (hit a pole/wall).

|

CASH

|

|

The repair cost is less than 2x your deductible.

|

CASH

|

|

You hit another person or their property.

|

CLAIM

|

|

There are any physical injuries reported.

|

CLAIM

|

|

You plan to sell the car in the next 12 months.

|

CASH (Avoids the Carfax "Accident" hit)

|

Strategic Links & Tools

Don’t let a minor dent ruin your retirement cash flow. Use our data-driven tools to make a “Bodyguard” decision.

- Benchmark Your Price: See the market floor for your zip code. 👉 Open Car Insurance Rate Estimator

- Discount Audit: Find the hidden senior credits you’ll lose if you file a claim. 👉 Open Senior Driver Discount Finder

Frequently Asked Questions (FAQ)

Often, yes. Many “Captive” agents are required to document every inquiry. That inquiry can show up as a “Zero-Dollar Claim” on your CLUE report. If you want to ask “What if,” call an Independent Broker or use our anonymous tools instead.

No. Most states and companies treat Comprehensive claims (Acts of God) much more leniently. Filing a claim for a cracked windshield or hail damage rarely results in a major surcharge, but it can affect your “Total Loss” status later.

This is tempting but risky. As your advocate, we warn: Get the cash at the scene via a digital app (Venmo/Zelle) or don’t do it. If you let them drive away promising to “send a check,” you will likely never see it.

Most policies give you 30 to 60 days to report an incident. This gives you plenty of time to get a cash estimate and run the math before involving the insurance company.

In many states, unfortunately, yes. While the surcharge is smaller for “Not-at-Fault” accidents, the insurance company may still move you to a slightly higher “Tier” because you are now statistically more likely to be involved in future incidents.

Check Your New Senior Rate Now (Stop the Bundle Trap. Protect your fixed income today.)