You have a perfect driving record. You haven’t had a ticket since the 1990s, and your last “fender bender” was ten years ago. You assume that your auto insurance company sees you as the “Gold Standard” of safe drivers.

But here is the sageWISE Warning: In 47 states, your driving record is only half the story. The other half is your Credit Score.

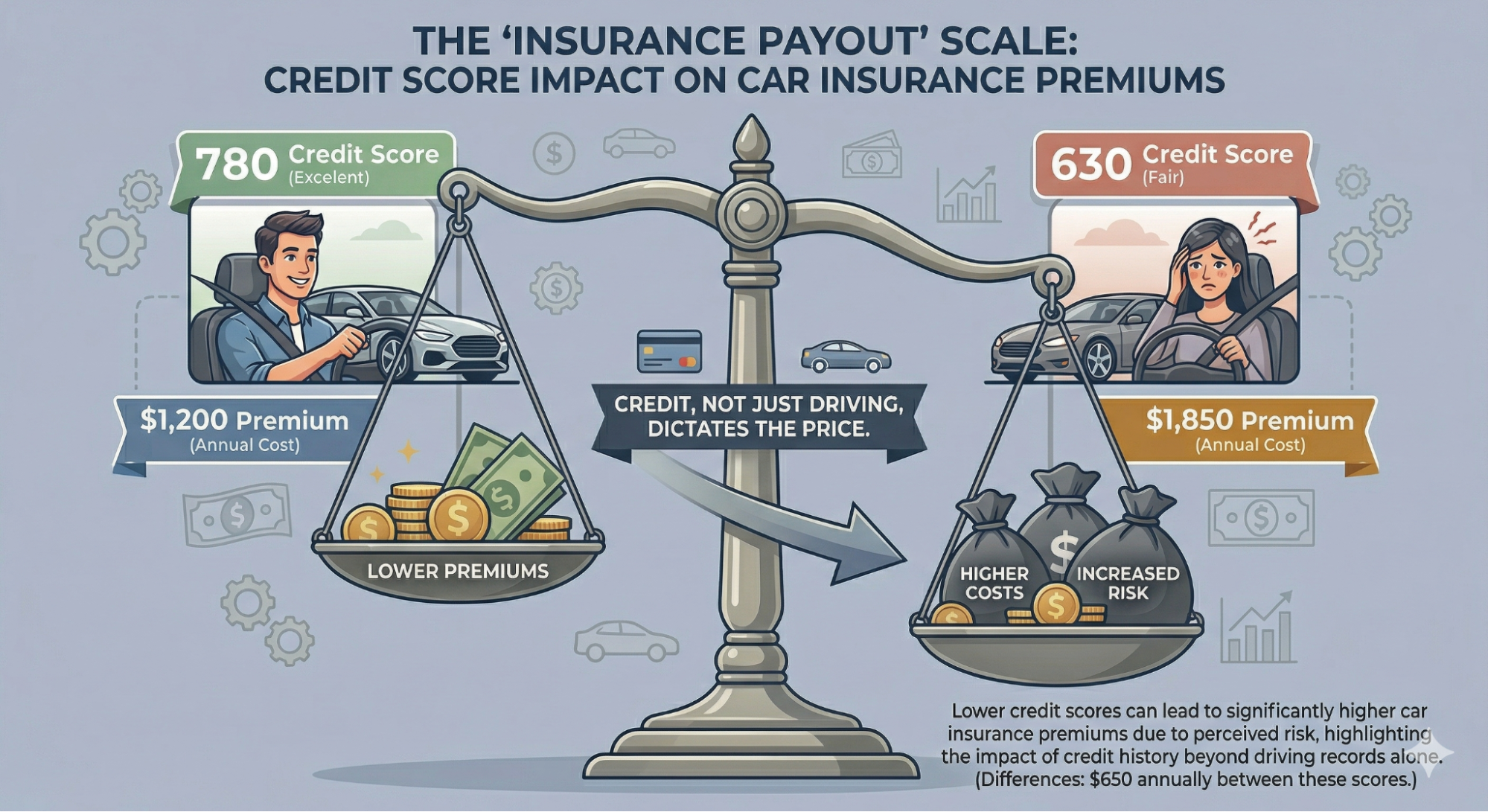

In the modern insurance industry, carriers use a “Credit-Based Insurance Score” (CBIS) to predict how likely you are to file a claim. To an actuary, a senior with a 620 credit score is a higher risk than a senior with an 800 score—even if the 620-score driver has never had an accident in their life. The industry’s data suggests that financial stability and driving safety are statistically linked.

As your trusted advocate, we have performed a Sagewise Audit of the 2026 credit-insurance nexus. We will show you the math of the “Credit Surcharge,” explain why a 50-point boost can save you $400 a year, and provide the exact steps to “Audit-Proof” your credit file before your next renewal.

Key Takeaways

- The CBIS Factor: Insurance companies use a specialized version of your credit report to set your “Tier” before they even look at your car.

- The 20% Swing: Moving from “Fair” to “Good” credit typically results in a 15% to 22% drop in annual premiums.

- State Protections: California, Hawaii, and Massachusetts are the only states that legally forbid insurers from using credit scores to set rates.

- The sageWISE Tip: If you have recently used a Debt Consolidation Loan to pay down credit card balances, you must re-shop your insurance immediately to claim your “Credit Refund.”

Stop paying a “Credit Penalty” on your car insurance. See if your new score qualifies you for a lower rate.

Check Your New Senior Rate Now

The sageWISE Audit: FICO vs. The Insurance Score

It is a common point of confusion: seniors think their “FICO Score” (used for mortgages) is the same as their “Insurance Score.” While they use the same raw data from Equifax, Experian, and TransUnion, the weighting is different.

A mortgage lender cares if you will pay your debt. An insurance company cares if you will file a claim.

How the Insurance Score is Weighted:

- Payment History (40%): Just like a regular score, the insurance company wants to see 10+ years of on-time payments. They view consistent bill-paying as a sign of a “low-stress” lifestyle, which leads to fewer accidents.

- Credit Utilization (30%): This is the biggest “lever” for seniors. If you are maxing out your credit cards, the insurer sees “Financial Distress,” which they correlate with higher risk-taking behavior.

- Length of Credit History (15%): This is the Senior Advantage. Your 40-year credit file is a massive shield that protects you from being placed in high-risk “New Driver” tiers.

- Types of Credit (10%): A mix of a mortgage, a car loan, and 1-2 credit cards is seen as the “Stable Ideal.”

The Math: What is a 50-Point Boost Worth?

To be your own financial bodyguard, you must understand the “Tier System.” Insurance companies group drivers into “Price Buckets.” Crossing the threshold into a higher bucket is where the massive savings occur.

Scenario: A Senior Driver with a 2019 Toyota Avalon.

|

Credit Tier

|

FICO Range

|

Avg. Annual Premium

|

Monthly Budget Impact

|

|---|---|---|---|

|

Poor

|

500 - 579

|

$2,850

|

$237.50

|

|

Fair

|

580 - 669

|

$2,100

|

$175.00

|

|

Good (The Goal)

|

670 - 739

|

**$1,650**

|

$137.50

|

|

Excellent

|

740 - 850

|

$1,320

|

$110.00

|

The Audit Result: Moving from the “Fair” bucket to the “Good” bucket—a simple 50-point increase—saves this senior $450 per year. If you achieve that boost and don’t re-shop your policy, you are voluntarily paying a “Credit Tax” to your current insurer.

3 "Bodyguard" Steps to Boost Your Score for Insurance

If your score is currently in the “Fair” range, use these three strategies to move the needle before your next six-month renewal.

1. The "Statement Date" Hack (Lowering Utilization)

As we noted in our guide Why Your Credit Score Dropped, the bureaus take a snapshot of your balance on your statement date, not your due date.

- The Move: Pay your credit card bill in full 3 days before the statement closing date. This reports a 0% or 1% utilization to the insurance computer, which can trigger an immediate 20 to 40-point score jump.

2. The "Credit Limit" Shield

If you carry a small balance and don’t want to pay it off yet, call your bank and ask for a Credit Limit Increase.

- The Logic: If you owe $1,000 on a $2,000 limit, you are at 50% utilization (High Risk). If you increase the limit to $5,000, that same $1,000 balance is only 20% utilization (Low Risk). The insurance company will reward you for the “Available Buffer.”

3. The "Error Audit"

According to the FTC, 1 in 5 people have errors on their credit reports. For a senior, this is often “Mixed File” data from a relative with a similar name.

- The Move: Check your report at AnnualCreditReport.com. If you find a late payment that isn’t yours, dispute it. Removing one false late payment can jump your score by 50+ points instantly, triggering a lower insurance tier.

Strategy: Re-Shopping the "Credit-Blind" Carriers

If you have a low credit score due to medical debt or a recent Holiday Debt Hangover, you shouldn’t be insured by a company like State Farm or Allstate, who weigh credit heavily.

Instead, you need an Independent Broker who can find “Credit-Lenient” carriers. Some regional companies or specialized senior mutuals weigh driving history much higher than credit. By moving to a company that ignores a 600-score, you can save $600 a year while you work on rebuilding your financial reputation.

Step-by-Step: How to Claim Your "Credit Refund"

Do not wait for your insurance company to notice your score went up. They won’t. You have to force the issue.

Step 1: Check Your Score

Use one of our Top 4 Free Credit Monitoring Tools to verify your current standing. If you see a jump of 30+ points, proceed to Step 2.

Step 2: Request a "Re-Rate"

Call your current agent. Ask: “My credit score has improved significantly since my last renewal. Can you perform a ‘Mid-Term Re-Rate’ to see if I qualify for a better tier?” Some companies will do this; many “Loyalty Tax” companies will refuse.

Step 3: Run the Estimator

If they refuse to re-rate you, use our Car Insurance Rate Estimator to find a new company that will recognize your improved status. Switching to a new company is the only way to ensure the most recent credit data is used in your pricing.

Frequently Asked Questions (FAQ)

In 47 states, yes. It is allowed under the Fair Credit Reporting Act (FCRA). The insurance company must have a “permissible purpose,” and setting a premium rate is considered one.

Insurance companies perform a “Soft Inquiry.” This is invisible to other lenders and has a 0.0 impact on your FICO score. You can shop for 20 different insurance quotes and your credit score will not drop by a single point.

Congratulations! California, Hawaii, and Massachusetts have banned the use of credit scores for auto insurance. If you live in these states, your rate is determined by your mileage, years of experience, and driving record. You are already shielded from the Credit Collision.

Unfortunately, yes. At your next renewal, many insurers will re-run your credit. If you’ve taken on new Secured Debt or missed a payment, they may move you to a more expensive “Standard” or “Non-Standard” tier.

Some small, local companies offer “No Credit” options, but they are almost always more expensive than a standard company’s “Good Credit” rate. They assume that if you don’t want your credit checked, it must be bad. Your best move is to use our Credit Building Guide to fix the score and then shop for “Preferred” rates.

Check Your New Senior Rate Now (Protect your reputation. Protect your rate. Stay in control of your budget today.)