The way you shop for auto insurance needs to change as you move into your senior years. Why? Because the factors that once raised your rates (like age) are now balanced by the factors that lower them (like years of safe driving).

Your priorities have also shifted. You’re no longer focused on “new car replacement” coverage. You need maximum savings, stability, and excellent claims service.

NerdWallet’s analysis is a great starting point, but we’ve filtered it for the needs of the mature driver. We assessed companies based on financial strength, claims handling, and the availability of senior-specific discounts.

Here is our short list of the top auto insurance companies for drivers aged 55 and older.

Key Takeaways

- You Should Be Paying Less: Mature drivers are often eligible for significant savings because of low mileage and safe driving history.

- Stability is Key: Focus on the company’s Financial Strength (A.M. Best Rating) and low Consumer Complaints—this guarantees they’ll be there when you file a claim.

- Best All-Around: Travelers consistently offers the best rates and senior discounts nationwide.

- Military/Veterans: USAA remains the cheapest option, but is restricted to military families.

The 5 Best Car Insurance Companies for Mature Drivers

The following companies all scored highly in our analysis, emphasizing stability and customer service over cheap rates for a young, risky driver. We focused on discounts that matter to you.

|

Insurer

|

Sagewise Rating

|

Best For

|

NAIC Complaints

|

|---|---|---|---|

|

Travelers

|

5.0

|

Best Overall Discounts & Rates

|

Far fewer than expected

|

|

State Farm

|

5.0

|

Best for Local Agent Support

|

Fewer than expected

|

|

American Family

|

5.0

|

Best for Claims Satisfaction

|

Far fewer than expected

|

|

USAA

|

5.0

|

Far fewer than expected

|

Far fewer than expected

|

Best Overall Discounts & Rates: Travelers

Sagewise Rating: 5.0 / 5.0

Why it’s one of the best: Travelers earned the best overall score out of the insurers we analyzed. They offer a broad range of coverage options and one of the largest discounts for retirees who reduce their annual mileage.

- Company Overview: Travelers is consistently rated highly for both financial stability and competitive pricing nationwide. They stand out because their rates are generally low across the board, and they offer one of the most substantial discounts if you are retired and now drive less than the national average. Their flexible policy options, including things like new car replacement coverage, are backed by strong customer service scores.

Best for Bundling (Home & Auto): Auto-Owners

Sagewise Rating: 5.0 / 5.0

Why it’s one of the best: Auto-Owners is an excellent choice for drivers who own their home and want to consolidate their insurance policies. Bundling with Auto-Owners minimizes fees and offers convenient one-stop customer service, including a rare common loss deductible benefit.

- Company Overview: Auto-Owners is a fantastic option for homeowners who value security and simplicity. Their multi-policy discounts are among the best in the industry, making the cost savings substantial when you bundle auto and home coverage. Furthermore, their reputation for claims handling is outstanding, giving seniors peace of mind that a simple call covers both their car and house in case of a disaster.

Best for Local Agent Support: State Farm

Sagewise Rating: 5.0 / 5.0

Why it’s one of the best: For drivers who prefer personalized service over an online application, State Farm is the market leader. Policies are sold exclusively through local agents, providing a human-touch customer support experience, which is valuable during the claims process.

- Company Overview: State Farm excels because it balances a massive national presence with local, personal service. Their policies are sold exclusively through dedicated agents, meaning you always have a specific person to call who knows your file and can walk you through the claims process step-by-step. This level of personalized support is invaluable to seniors who prefer speaking to a person over navigating an automated phone system.

Best for Claims Satisfaction: American Family

Sagewise Rating: 5.0 / 5.0

Why it’s one of the best: American Family consistently ranks near the top for customer satisfaction, specifically regarding the claims experience. Their track record for simplifying that process minimizes stress after an accident.

- Company Overview: American Family earns its high marks by focusing on the moment that truly matters: when you have an accident. Their commitment to streamlining the claims process means less paperwork, fewer delays, and clear communication. For the mature driver, knowing that their claim will be processed quickly and fairly, without undue stress or complication, is a core benefit.

Best for Military & Veterans: USAA

Sagewise Rating: 5.0 / 5.0

Why it’s one of the best: For active military, veterans, and their families, USAA is virtually unbeatable on price and service. They consistently earn high marks for their customer satisfaction and claims service.

- Company Overview: USAA provides highly competitive rates and exclusive perks tailored to the military community. Their customer base consistently rates their claims process and overall service satisfaction as industry-leading. This high-level service, combined with military-specific benefits and excellent financial stability, makes them the non-negotiable choice for those who qualify for membership.

The Claims Service Difference: What Truly Matters to a Senior

The biggest worry about auto insurance isn’t the price; it’s the fear of a difficult, complicated claims process when you’re under stress.

A good insurance company shouldn’t just be cheap—it should be reliable.

- Look at Complaints: We prioritize companies with low complaint ratios (like Auto-Owners and American Family). This is the best indicator that they will process your claim quickly and fairly.

- Check Financial Strength: Financial strength (A.M. Best rating of A or higher) ensures the company has the massive reserves needed to pay large claims quickly, without delays or pushback.

Your Senior Auto Insurance Audit Checklist

Use this comprehensive checklist to ensure you are not overpaying and that you have the right coverage for your lifestyle.

- [ ] 1. Have I claimed my Low-Mileage Discount?

- Action: If you are retired and drive less than 7,500 miles a year, you are eligible for one of the largest discounts available. Contact your agent to report your annual mileage.

- [ ] 2. Have I checked for a Defensive Driving Discount?

- Action: Completing a state-approved defensive driving course (often online or at a local community center) can earn you a discount that lasts for years.

- [ ] 3. Am I maximizing my Bundling Discount?

- Action: Bundling your auto and home insurance with one company (like Auto-Owners) is the fastest way to save 10% to 20% immediately.

- [ ] 4. Is my Collision Coverage still necessary?

- Action: If your car is 10 years old or older and has a low market value (say, under $4,000), calculate if dropping Collision/Comprehensive coverage would save you more than the car is worth. This is usually a smart financial move.

- [ ] 5. Have I raised my Deductible?

- Action: Increasing your deductible from $500 to $1,000 can significantly lower your monthly premium. Use the money you save to build up your emergency fund.

- [ ] 6. Have I shopped for quotes in the last two years?

- Action: Insurance companies rely on loyalty to quietly raise rates. The only way to ensure you keep the maximum discount is to compare quotes from three to five companies every two years.

The Financial Connection (Auto Savings & Home Equity)

For homeowners, there’s a powerful opportunity to maximize the money you save on your auto premiums by linking it directly to your home’s financial power.

The average homeowner over 65 has substantial equity—often their single largest, most valuable asset. This money is just sitting there, not working. Smart financial planning involves looking at your entire budget holistically, turning small savings into a catalyst for accessing major wealth.

The Two-Part Strategy

1. Step One: Generate “Found Money” from Your Car

First, you must create the savings buffer. By using our Audit Checklist, you can typically reduce your monthly auto premium by $30 to $50 (or more). This money, which you were wasting on overpriced insurance, is now “found money” that can be strategically redirected.

2. Step Two: Access Home Cash with Confidence

You can use the monthly auto savings generated in Step 1 to offset the costs of accessing your home’s wealth. Tools like a Home Equity Line of Credit (HELOC) or a Reverse Mortgage are designed to provide tax-free funds or eliminate mortgage payments entirely, freeing up major monthly income.

- Reverse Mortgage (HECM): This tool is ideal for eliminating monthly housing payments. It pays off your existing mortgage and can provide you with a tax-free monthly income stream or line of credit for life. The goal is to maximize your monthly cash flow and eliminate the largest fixed expense most seniors have.

- Home Equity Line of Credit (HELOC): This is a flexible line of credit you can tap when needed, allowing you to access cash for emergencies or planned expenses (like home modifications). It keeps your home and car assets working together to create a necessary safety net.

If you are already reviewing your home and auto insurance, it’s the perfect time to review how you can safely and strategically access your most valuable asset—your home’s equity—to build long-term financial security.

How We Rate the Best Auto Insurance Companies for Seniors

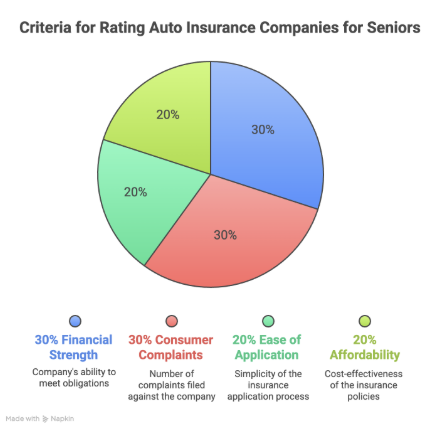

At Sagewise, our ratings are focused on what matters to a senior. We are not looking for the cheapest rate for a 25-year-old; we are looking for stability, claims reliability, and maximum senior savings. To earn our top ratings, a company must excel at these four core categories. We analyze these factors using public data and weigh them based on the specific needs of the mature driver.

- Financial Strength (30%): We use AM Best ratings. A life insurance policy is a long-term promise, and this “grade” proves a company is financially sound and will be there to pay the claim for your family, even decades from now. This is non-negotiable for us. We prioritize companies with an “A” rating (Excellent) or higher.

- Ease of Application (20%): We give higher scores to companies that make it simple for seniors to get coverage. We look for simple applications, fast processing, and a high degree of transparency on their website.

- Consumer Complaints (30%): We check the National Association of Insurance Commissioners (NAIC) complaint index. This data shows if a company pays claims fairly and on time, or if they have a history of fighting with beneficiaries. A low complaint ratio is the strongest indicator of a smooth, hassle-free payout.

- Affordability (20%): We score companies on their average rates combined with the availability of senior-specific discounts (e.g., low mileage, safe driving).

Easily compare personalized rates to see how much switching car insurance could save you

Frequently Asked Questions (FAQ)

Rates sometimes increase slightly after age 75 because statistics show that drivers in this age group are statistically more likely to be involved in certain types of accidents. However, the savings from low-mileage and safe driving often offset this completely.

It is safe if you have the savings to replace the car yourself. If the premium you are paying annually for collision is more than 10% of the car’s current market value, dropping the coverage is usually a smart financial move.

Yes, in most states. Insurers use a “credit-based insurance score” to predict the likelihood of you filing a claim. Improving your credit score can often lead to savings on your auto insurance premiums.

This depends on your preference. Companies like State Farm offer local agents who provide personal, human support (great for claims). Companies like Travelers or GEICO offer great online rates and apps (great for convenience). You should get quotes from both to compare the final price.

You should review your policy and coverage levels once a year to ensure you aren’t overinsured, and you should shop around for quotes every two to three years to prevent the insurance company from gradually raising your rate.