For drivers over 60, car insurance should be getting cheaper, not more expensive. If you are still paying for the same coverage you bought when you were working full-time, you are likely wasting money.

Your financial goals have changed. You need to switch from full coverage (which is expensive and often unnecessary for an older car) to liability coverage supplemented by your senior-specific discounts.

This guide cuts through the complicated rates and shows you exactly how to find the maximum savings without sacrificing stability.

Key Takeaways

- Liability is the Goal: For older, low-value cars, dropping Collision and Comprehensive (Full Coverage) is the fastest way to save.

- Low Mileage is Gold: Retirees who drive less than 7,500 miles/year qualify for one of the largest discounts available.

- Travelers offers the best national average rates for seniors, but always compare prices.

- USAA is the cheapest overall, but is restricted to military families.

Full Coverage vs. Liability: Which is Right for You?

This is the single most important decision a mature driver can make to save money.

|

Coverage Type

|

What It Is

|

Who Should Use It

|

|---|---|---|

|

Full Coverage

|

The Most Expensive. A combination of Collision, Comprehensive, and Liability.

|

Required if you have a car loan or lease. Recommended if you own a newer car or one worth more than $10,000.

|

The Cheapest Auto Insurance for Seniors (70-Year-Old Profile)

The chart below shows the lowest national average rates for full coverage (which is what most companies publish). Always assume your rate will be lower because of your good driving history and low mileage.

|

Company

|

Median Annual Rate

|

Median Monthly Rate

|

Why They Are Cheap

|

|---|---|---|---|

|

Travelers

|

$1,642

|

$137

|

Best for Low-Mileage Drivers

|

Why These 5 Companies Are Cheapest for Seniors

The secret to saving money isn’t just comparing the final price; it’s understanding the unique strengths of each company and how they reward the mature driver.

1. Travelers: The Low-Mileage Winner

Travelers is consistently the cheapest company for the general senior population who are not military-affiliated. This is primarily because they offer one of the most substantial and easily accessed low-mileage discounts. If you have retired and significantly reduced your annual driving, Travelers’ algorithm rewards this behavior with rock-bottom rates. They are highly efficient for getting an online quote quickly.

2. USAA: The Undisputed Cheapest

For active military, veterans, and their families, USAA offers rates that are virtually impossible for any other major carrier to beat. If you qualify for membership, their rates are the gold standard for affordability, and they back it up with top-tier claims service.

3. GEICO: The Liability Leader

GEICO is the strongest option for seniors who have made the smart financial decision to carry only Liability Coverage on their older, paid-off vehicle. Their minimum coverage rates are among the lowest in the nation, making them the default choice for seniors who are focused entirely on saving money on their monthly premium.

4. State Farm: The Defensive Driver Specialist

State Farm is a strong fit for seniors who have recently completed (or plan to complete) a state-approved defensive driving course. State Farm frequently offers one of the best discounts for this specific activity. Their local agent model ensures that this discount is properly applied to your policy immediately.

5. Auto-Owners: The Homeowner’s Choice

Auto-Owners provides excellent rates if you own your home, because their primary goal is to bundle your home and auto policies. For a senior seeking simple, reliable, and consolidated billing, Auto-Owners’ multi-policy discount often makes them the best overall value once all premiums are combined.

Cheapest Rates by Age Group (The Traveler's Example)

Your age and life stage dramatically impact your rates. The good news is, being a retiree puts you in one of the cheapest groups.

|

Driver Age

|

Life Stage

|

Median Monthly Rate

|

|---|---|---|

|

20-Year-Old

|

Inexperienced, High Risk

|

$307

|

The Best Savings Strategy: Focus on Liability

For a senior looking to save the absolute maximum amount of money, the cheapest policy will always be Liability Coverage.

|

Company

|

Median Monthly Rate (Liability Only)

|

|---|---|

|

USAA*

|

$32

|

|

$45

|

Warning: While cheap, your state’s minimum liability coverage may not be enough to cover you if you cause a serious accident. If you cause $50,000 in damage, but your policy only covers $25,000, you are personally liable for the rest. If you choose liability-only coverage, ensure you buy coverage limits that protect your assets.

Audit Your Discounts: How to Get Maximum Savings

The best way to save is to combine several discounts that reward maturity. Never assume your insurer has applied these automatically—you must ask for them!

- Claim Your Low-Mileage Discount (The Retiree Goldmine):

- Detail: If you are retired and drive less than 7,500 miles a year (the national average is 13,500), you are eligible for one of the largest single discounts available. This reflects a significant reduction in risk for the insurer.

- Action: Contact your agent and ask to report your actual annual mileage. This discount alone can offset any rate increases you see due to age.

- Take a Defensive Driving Course (The Safety Discount):

- Detail: Completing a state-approved defensive driving or accident prevention course (often available online or at a local community center) proves you are actively committed to safe driving. This is a common and easy discount to claim and lasts for years.

- Action: Ask your insurer which specific courses they approve in your state before enrolling.

- Raise Your Deductible (The Cash Flow Fix):

- Detail: Your deductible is the amount you pay out-of-pocket before insurance pays for a claim. Increasing your deductible from $500 to $1,000 can significantly lower your monthly premium because you are taking on more initial risk.

- Action: Calculate the monthly savings. Use that money to build up your emergency fund, which is a better use of cash on a fixed income.

- Bundle Your Policies (The Simplest Savings):

- Detail: Insuring your car and home with the same company is the fastest, simplest way to save 10% to 20% immediately with virtually no effort. Companies like Auto-Owners specialize in maximizing this benefit.

- Action: Get a single quote for both auto and home from 2–3 different companies and compare the final bundled price.

The Financial Connection (Auto Savings & Home Equity)

For homeowners, there’s a smart way to maximize the money you save on your auto premiums.

The average homeowner over 65 has substantial equity. That equity can be accessed to create cash flow using tools like a Home Equity Line of Credit (HELOC) or a Reverse Mortgage.

The Strategy:

- Reduce Auto Premiums: Use our Audit Checklist to reduce your monthly premium by $30-$50.

- Access Home Cash: Use the money saved on your car insurance to offset the costs of accessing your home’s wealth. Tools like a HELOC or a Reverse Mortgage can provide tax-free funds or eliminate mortgage payments entirely, freeing up major monthly income.

If you are already reviewing your home and auto insurance, it’s the perfect time to review how you can access your most valuable asset—your home’s equity.

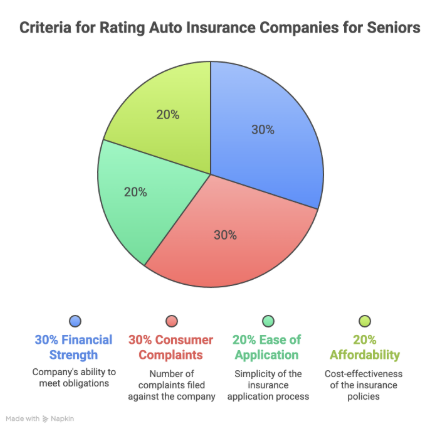

How We Rate the Best Auto Insurance Companies for Seniors

At Sagewise, our ratings are focused on what matters to a senior. We are not looking for the cheapest rate for a 25-year-old; we are looking for stability, claims reliability, and maximum senior savings. To earn our top ratings, a company must excel at these four core categories. We analyze these factors using public data and weigh them based on the specific needs of the mature driver.

- Financial Strength (30%): We use AM Best ratings. A life insurance policy is a long-term promise, and this “grade” proves a company is financially sound and will be there to pay the claim for your family, even decades from now. This is non-negotiable for us. We prioritize companies with an “A” rating (Excellent) or higher.

- Ease of Application (20%): We give higher scores to companies that make it simple for seniors to get coverage. We look for simple applications, fast processing, and a high degree of transparency on their website.

- Consumer Complaints (30%): We check the National Association of Insurance Commissioners (NAIC) complaint index. This data shows if a company pays claims fairly and on time, or if they have a history of fighting with beneficiaries. A low complaint ratio is the strongest indicator of a smooth, hassle-free payout.

- Affordability (20%): We score companies on their average rates combined with the availability of senior-specific discounts (e.g., low mileage, safe driving).

Your Senior Auto Insurance Audit Checklist

Use this comprehensive checklist to ensure you are not overpaying and that you have the right coverage for your lifestyle.

- [ ] 1. Have I claimed my Low-Mileage Discount?

- Action: If you are retired and drive less than 7,500 miles a year, you are eligible for one of the largest discounts available. Contact your agent to report your annual mileage.

- [ ] 2. Have I checked for a Defensive Driving Discount?

- Action: Completing a state-approved defensive driving course (often online or at a local community center) can earn you a discount that lasts for years.

- [ ] 3. Am I maximizing my Bundling Discount?

- Action: Bundling your auto and home insurance with one company (like Auto-Owners) is the fastest way to save 10% to 20% immediately.

- [ ] 4. Is my Collision Coverage still necessary?

- Action: If your car is 10 years old or older and has a low market value (say, under $4,000), calculate if dropping Collision/Comprehensive coverage would save you more than the car is worth. This is usually a smart financial move.

- [ ] 5. Have I raised my Deductible?

- Action: Increasing your deductible from $500 to $1,000 can significantly lower your monthly premium. Use the money you save to build up your emergency fund.

- [ ] 6. Have I shopped for quotes in the last two years?

- Action: Insurance companies rely on loyalty to quietly raise rates. The only way to ensure you keep the maximum discount is to compare quotes from three to five companies every two years.

- [ ] 1. Have I claimed my Low-Mileage Discount?

Easily compare personalized rates to see how much switching car insurance could save you

Frequently Asked Questions (FAQ)

Rates sometimes increase slightly after age 75 because statistics show that drivers in this age group are statistically more likely to be involved in certain types of accidents. However, the savings from low-mileage and safe driving often offset this completely.

It is safe if you have the savings to replace the car yourself. If the premium you are paying annually for collision is more than 10% of the car’s current market value, dropping the coverage is usually a smart financial move.

Yes, in most states. Insurers use a “credit-based insurance score” to predict the likelihood of you filing a claim. Improving your credit score can often lead to savings on your auto insurance premiums.

This depends on your preference. Companies like State Farm offer local agents who provide personal, human support (great for claims). Companies like Travelers or GEICO offer great online rates and apps (great for convenience). You should get quotes from both to compare the final price.

You should review your policy and coverage levels once a year to ensure you aren’t overinsured, and you should shop around for quotes every two to three years to prevent the insurance company from gradually raising your rate.