For a senior on a fixed income, inflation isn’t just a news headline—it’s a monthly pay cut. When the price of eggs, milk, and gasoline goes up, your Social Security check doesn’t stretch as far.

You can’t control the price at the pump, but you can control how you pay.

If you are paying with cash or a debit card, you are paying full retail price. By switching to the right No-Annual-Fee Cash Back Credit Card, you can effectively give yourself a permanent 3% to 5% discount on your two biggest expenses.

As your trusted advocate, we are here to show you which cards offer the best returns on “survival spending” and how to use them safely to keep more money in your pocket.

Key Takeaways

- The Strategy: Use a specific credit card only for gas and groceries to earn maximum cash back.

- The Rule: You must pay the balance in full every month. If you pay interest, you lose the benefit.

- Best for Both: The Amex Blue Cash Everyday® is our top pick for earning 3% on both gas and groceries with no fee.

- Best for One: The Citi Custom Cash® offers a massive 5% back on your top spending category (like gas).

Quick Comparison: Top Cards for Essential Spending

Use this table to quickly find the card that matches your spending habits.

|

Card Name

|

Best For

|

Gas/Grocery Reward

|

Official Link

|

|---|---|---|---|

|

Blue Cash Everyday® (Amex)

|

Simplicity (Both)

|

3% on Groceries & Gas

|

|

|

Effectiveness

Citi Custom Cash®

|

Max Savings (One Category)

|

5% on your top category (up to $500/mo)

|

|

|

Capital One SavorOne

|

Food & Dining

|

3% on Groceries & Dining

|

The 'Inflation Offset' Strategy: How to Pay One Bill for Free

Don’t just let your cash back sit there. Use it strategically to “erase” inflation from your budget.

The Scenario: You spend $500/month on groceries and $150/month on gas.

- Using Cash/Debit: You get $0 back.

- Using the Amex Blue Cash Everyday: You earn 3% back ($19.50/month).

The Result: Over a year, that is $234 in free money. That is enough to pay for two months of your electric bill or cover your entire Netflix subscription for the year.

The 5-Year Impact: If you consistently use this strategy, the numbers get huge.

- 1 Year: $234 Saved

- 5 Years: $1,170 Saved (That’s a new appliance, a flight to see grandkids, or an emergency repair fund—created from thin air).

The 'Stacking' Secret: How to Save 15% on Groceries

The real power comes when you combine your card with existing senior perks. This is the “Stacking Strategy.”

- Find a Senior Discount Day: Many chains (like Harris Teeter, Fred Meyer, Hy-Vee, or Publix) offer a 5% or 10% senior discount on specific days (usually Tuesdays or Thursdays).

- Pay with Your 5% Card: Use a high-reward card like the Citi Custom Cash.

- The Result: You aren’t just saving 5%; you are saving 15% total on your grocery bill. On a $200 trip, that’s $30 back in your pocket instantly.

1. Top Pick: Best for “Set It and Forget It” (Gas & Groceries)

Card: Blue Cash Everyday® Card from American Express

- Sagewise Rating: 5.0/5.0

- Why it wins for Seniors: It is the definition of simplicity. You don’t have to choose between food and fuel; it covers both.

- The Rewards:

- 3% Cash Back at U.S. supermarkets (up to $6,000 per year).

- 3% Cash Back at U.S. gas stations (unlimited).

- 3% Cash Back on U.S. online retail purchases (great for Amazon or medical supplies).

- Annual Fee: $0.

Check Rates at American Express

2. Top Pick: Best for “High Spenders” (5% on One Category)

Card: Citi Custom Cash® Card

- Sagewise Rating: 4.5/5.0

- Why it wins for Seniors: It automatically adapts to you. If you have a month where you drive a lot (a road trip to see grandkids), it becomes your “Gas Card.” If you are hosting a holiday dinner, it becomes your “Grocery Card.”

- The Rewards: 5% Cash Back on your top eligible spend category each billing cycle (up to the first $500 spent).

- Annual Fee: $0.

- Strategic Tip: Use this card only for your biggest expense (e.g., just for groceries) to guarantee you get the full 5% back.

The Wholesale Club Warning

This is where many seniors get trapped. If you buy your gas and groceries at Costco, Sam’s Club, or BJ’s, most standard “Gas & Grocery” cards will not work.

- The Issue: Credit card networks code these stores as “Wholesale Clubs,” not “Supermarkets” or “Gas Stations.” A card like the Amex Blue Cash Everyday will only give you 1% back here.

- The Fix: If you are a loyal club shopper, you need a specialized strategy.

- For Costco: You must use a Visa card (like the Costco Anywhere Visa®) to get 4% on gas.

- For Sam’s Club: The Sam’s Club Mastercard offers 5% on gas.

- The Strategy: Do not use your standard grocery card at the warehouse club; you are leaving money on the table.

Security Alert: Essential Features for Seniors

Seniors are frequently targeted by scammers. The credit card you choose should be your first line of defense. All the cards on our list include these three non-negotiable safety features:

- $0 Fraud Liability: If your card is lost, stolen, or used online without your permission, you are legally not responsible for a single penny of the unauthorized charges.

- Instant Transaction Alerts: You can set up the card to send a text message to your phone immediately every time a purchase is made. This is the fastest way to spot a thief.

US-Based Customer Support: When there is a problem, you need to be able to hear and understand the person helping you. Premium cards (like Discover and Amex) are famous for their clear, helpful support teams.

Which Spender Are You? Finding Your Perfect Match

Still not sure? Find your “Spender Personality” below to see which card fits your lifestyle.

|

If you are...

|

Your Goal Is...

|

The Best Card Is...

|

|---|---|---|

|

The Home Chef

|

Saving on weekly grocery runs and gas fill-ups.

|

Amex Blue Cash Everyday

|

|

The "Set it and Forget it"

|

Getting a good deal without tracking categories.

|

Citi Double Cash

|

|

The Socializer

|

Dining out with friends and picking up prescriptions.

|

Chase Freedom Unlimited

|

|

The Snowbird/Traveler

|

Avoiding fees while traveling or cruising abroad.

|

Capital One Quicksilver

|

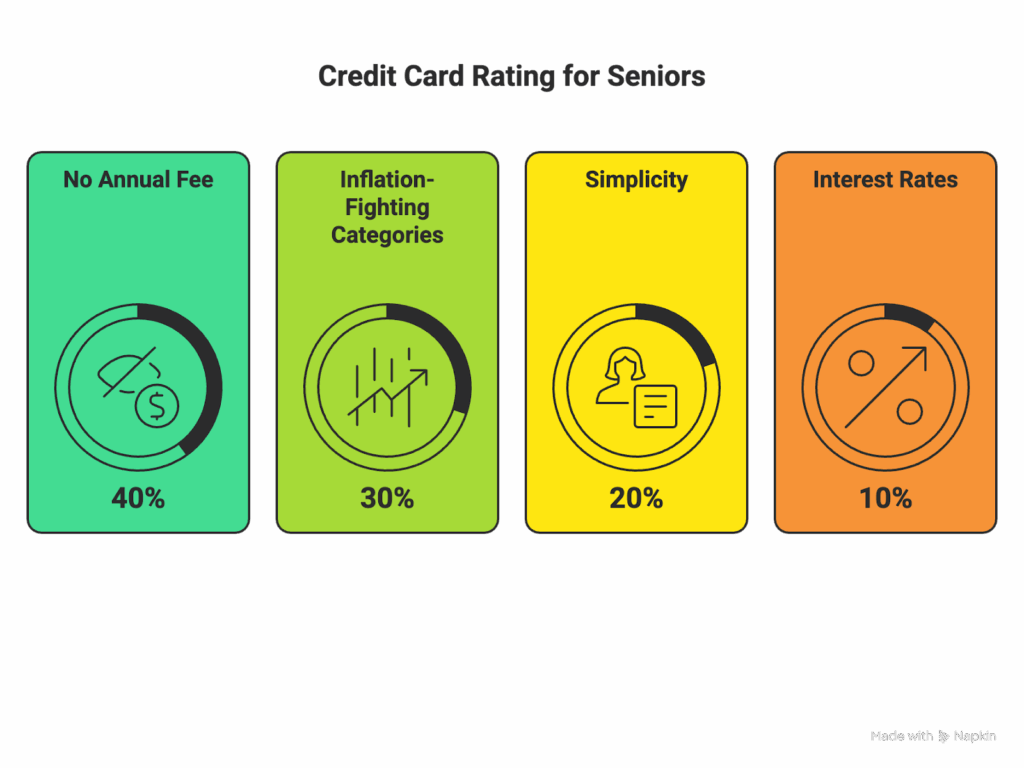

How We Rate Credit Cards for Seniors

At Sagewise, we ignore the “flashy” perks like airport lounges or travel points that require complex transfers. We focus on the financial reality of a fixed income. We weigh these factors:

- No Annual Fee (40%): We believe seniors should not pay for the privilege of using a credit card. All our top picks are free to hold.

- Inflation-Fighting Categories (30%): We prioritize cards that give high cash back (3%+) on necessities like food, gas, and medicine.

- Simplicity (20%): We favor cards with easy redemption processes (cash or statement credits) over complex point systems.

- Interest Rates (10%): While we advise paying in full, we look for cards that offer competitive APRs or 0% introductory periods for emergencies.

The "Debt Trap" Warning: When NOT to Do This

We must be honest: Rewards cards are dangerous if used incorrectly. The interest rates on rewards cards are often high (20% – 29%).

The Golden Rule: You must pay your statement balance in full and on time every single month.

- If you pay in full: You pay $0 in interest. The rewards are free money.

- If you carry a balance: The interest you pay will be far higher than the cash back you earn. You will lose money.

If you currently have credit card debt: Do not focus on rewards. Focus on a 0% Balance Transfer Card to eliminate the interest.

Your ‘Wallet Audit’ Checklist

Do you have the right tools in your wallet? Use this checklist to see if you are maximizing your discounts.

- [ ] 1. Do I have a “Grocery” card?

- Goal: You should be earning at least 3% back on every supermarket trip. (Recommendation: Amex Blue Cash Everyday)

- [ ] 2. Do I have a “Pharmacy” card?

- Goal: If you spend more than $100/month at the drugstore, you should be earning 3% back. (Recommendation: Chase Freedom Unlimited)

- [ ] 3. Do I have a “Catch-All” card?

- Goal: For everything else (utilities, insurance premiums, clothes), you should earn a flat 2%. (Recommendation: Citi Double Cash)

- [ ] 4. Am I paying an Annual Fee?

- Action: If you are paying $95+ a year for a card you rarely use for travel perks, cancel or downgrade it to a no-fee version immediately.

- [ ] 1. Do I have a “Grocery” card?

Frequently Asked Questions (FAQ)

es, slightly and temporarily. When you apply, the bank does a “hard pull” on your credit, which may drop your score by 5-10 points. However, if you pay on time and keep your balance low, your score will typically recover quickly and may even increase due to having more available credit.

No. If you carry a balance, the interest rate (often 20%+) will completely wipe out any 2% or 3% cash back you earn. If you have debt, ignore rewards and focus on finding a Low Interest or 0% Balance Transfer card to pay off the principal.

It’s very simple. Most banks allow you to apply your cash back as a “Statement Credit.” This means they simply reduce your monthly bill by the amount of cash you earned. It’s the easiest way to save.

This is an important estate planning question. Generally, if you are the sole account holder, your points or cash back balance expire with you; they are not transferable to heirs. It is a smart habit to redeem your cash back monthly rather than letting it stockpile, so you never lose the value you’ve earned.

Yes! The smartest strategy is to pair them. Use the Amex for groceries and gas, the Chase card for dining and pharmacy, and the Citi card for everything else. This ensures you are getting the maximum discount on every single purchase.

Find the Best Credit Card Rates (Start saving on every purchase today.)