You’ve worked your whole life to build your nest egg. You’ve saved in your 401(k) and your savings accounts. But now that you’re in or near retirement, you face one big, lingering question: “Will my money last?”

What if you live to be 95? This is the core fear that keeps many seniors up at night.

An annuity is one of the only financial tools in the world designed to solve this one specific problem.

It is not a magical, get-rich-quick investment. It is a simple tool of protection. This guide will explain, in plain English, what an annuity is and how it can help you create a guaranteed paycheck for life.

Key Takeaways

- It’s a “Personal Pension”: An annuity is a simple contract. You give an insurer a lump sum, and they send you a guaranteed monthly check for life.

- It Solves the #1 Fear: An annuity’s primary purpose is to ensure you cannot outlive your income.

- Simple is Safe: A “Fixed Annuity” is the safest, most predictable option for seniors, as it’s not tied to the stock market.

- It’s a Trade-Off: The main downside is “loss of liquidity.” You are trading access to your lump sum for the guarantee of lifelong income.

What is an Annuity? (A Simple Definition)

An annuity isn’t an “investment” in the way a stock is. It’s an “income insurance” contract you buy for your retirement.

Think of it this way:

- The Problem: Your #1 fear in retirement is, “What if I live to 95 and my 401(k) runs out of money?”

- The Solution: An annuity is the only financial product designed to solve this one specific problem.

It’s a simple, two-step contract you make with a high-rated insurance company:

- You Pay: You give them a lump sum of money (from your 401(k) or savings).

- They Pay You: In return, they agree to send you a guaranteed monthly paycheck for the rest of your life.

That’s it. You are not “investing” in the stock market; you are buying a guarantee. You are transferring the risk of “living too long” from yourself to the insurance company, so you never have to worry about your core income running out.

The 2 Payout Types: Immediate vs. Deferred

“Annuity” is a broad term. For seniors, the first choice you’ll make is when you want your paychecks to start.

- 1. Immediate Annuity (The “Start Now” Plan)

- How it works: This is the most straightforward option. You give the insurance company your lump sum (from a 401k or savings), and your guaranteed paychecks start next month.

- Who it’s for: A senior who is retiring today and needs to turn their savings into a stable, predictable income now.

- 2. Deferred Annuity (The “Start Later” Plan)

- How it works: This is a “buy it now, use it later” plan. You give the company your money today, and you “defer” (delay) taking the payments for several years (e.g., 5, 10, or 15 years). Because your money has time to grow, your future paychecks will be larger.

Who it’s for: A senior who is 60, still working, but wants to “lock in” a guaranteed income stream that will start when they turn 70.

The Most Important Choice: Fixed vs. Variable (Safety vs. Risk)

This is the most critical part of your decision. It’s the choice between “guaranteed and safe” or “risky and complex.”

- 1. Fixed Annuity (The Safe Path – Our Recommendation)

- How it works: Your money is not in the stock market. The insurance company gives you a guaranteed, fixed interest rate (like a CD). You will know, down to the penny, exactly how much your paycheck will be every month.

- Risk Level: Low. Your payout is 100% predictable.

- 2. Variable & Indexed Annuities (The Complex, Risky Path)

- How it works: These are high-fee products tied to the stock market. They promise a chance at higher returns but come with market risk and a confusing, 100-page contract.

- Risk Level: High. Your payout is not guaranteed to grow.

Our Honest Advice: For 99% of seniors, the goal of an annuity is to reduce risk, not add to it. A simple Fixed Annuity provides the peace of mind that these complex products cannot.

Your 3-Question 'Is an Annuity Right for Me?' Guide

An annuity is a big commitment. Use this simple 3-question guide to see if your goals align with what this tool is built to do.

Read the two options for each question and check the box that best describes your goals for this specific portion of your savings.

- What is this money’s primary “job”?

- [ ] (A) Its job is to be an “Emergency Fund.” My #1 priority is keeping this money safe and accessible for a new roof, a medical bill, or to help my family.

- [ ] (B) Its job is to be a “Paycheck.” My #1 priority is to turn this lump sum into a guaranteed monthly income that I cannot outlive.

- What is your “Liquidity” (Access to Cash) preference?

- [ ] (A) I am not comfortable locking up my money. I need to be able to get my full principal back at any time. I am not willing to pay a “surrender charge.”

- [ ] (B) I am comfortable locking up this money. I am willing to trade access to my lump sum in exchange for a 100% guarantee that my paycheck will never run out.

- What is your core “Peace of Mind” goal?

- [ ] (A) My goal is to protect this lump sum and pass the full amount on to my children. I am worried about the stock market, so I want it in a CD or savings.

- [S ] (B) My goal is to protect my income. I am worried about outliving my savings and becoming a financial burden on my children.

How to Read Your Results

- If you checked one or more “(A)” answers: An annuity is likely NOT the right tool for this specific pot of money. Your goals are focused on liquidity and savings (which is what a high-yield savings account or a CD is for). You should not lock up your emergency fund in an annuity.

- If you checked all three “(B)” answers: An annuity is a very strong fit for your goals. You have the right mindset: you are “insuring” your income, not just “investing” it. You’re ready for the peace of mind that a guaranteed, lifelong paycheck provides.

How Much Does a $100,000 Annuity Pay Per Month?

This is the real-world question. The answer depends on three factors:

- Your Age: The older you are when you start, the higher your monthly check.

- Your Gender: Since women have a longer life expectancy, their monthly payments are slightly lower than a man’s of the same age.

- Interest Rates: The higher the interest rates are when you buy, the higher your payout.

Example: A 65-year-old man who puts in $100,000 might get a guaranteed monthly check of $650 – $700 for the rest of his life. *A 65-year-old woman might get *$620 – $670* for the rest of her life.*

Annuity Payout Estimator

Estimate your potential monthly payout from a single-premium immediate annuity (SPIA).

This is a hypothetical estimate for illustrative purposes only. Not a quote or guarantee.

How Are Annuities Taxed? (The Simple Version)

This depends entirely on what money you used to buy it.

- If you use “Qualified” (Pre-Tax) Money (from a 401k or IRA): You haven’t paid taxes on this money yet. Your entire annuity check will be taxed as regular income, just like your 401(k) withdrawals would have been.

- If you use “Non-Qualified” (Post-Tax) Money (from a savings account or CD): You already paid taxes on this money. You will only pay taxes on the interest it earns. The insurance company handles this for you and will clearly state on your 1099 tax form how much is “principal” (non-taxed) and how much is “earnings” (taxed).

The Honest Pros vs. Cons for a Senior

An annuity is a powerful tool, but it’s a big decision. Here are the honest trade-offs.

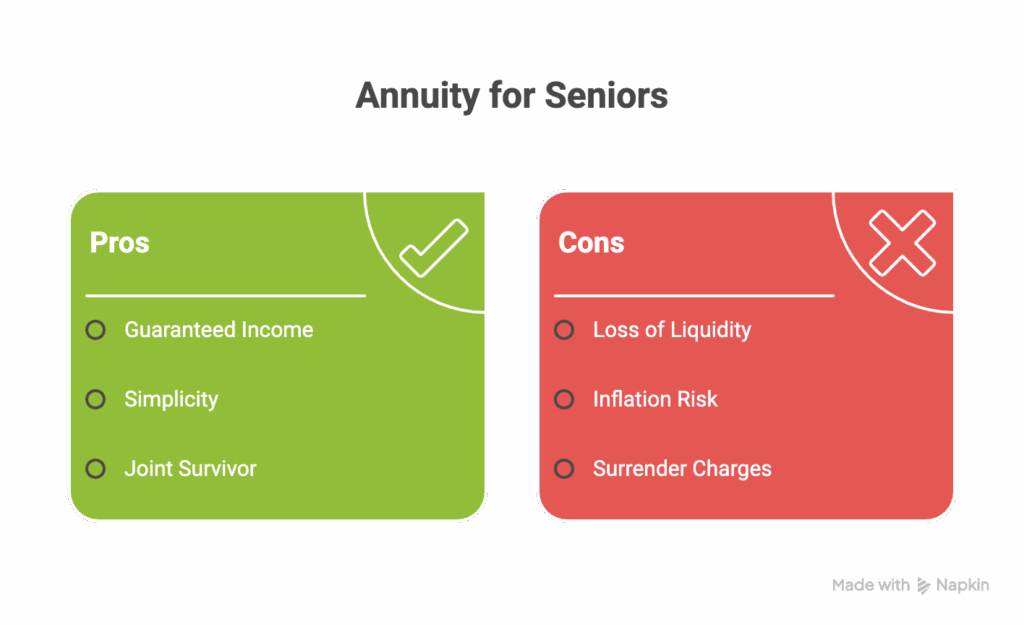

THE PROS:

- Guaranteed Income for Life: This is the #1 benefit. It is a 100% predictable paycheck. You cannot outlive it.

- Simplicity & No More Stress: A fixed annuity removes all stock market risk. You never have to watch the news and worry about your “investments.”

- Joint Survivor Option: You can set it up so that when you pass away, your spouse continues to get the same monthly check for the rest of their life.

THE CONS (THE “TRADE-OFFS”):

- Loss of Liquidity (The #1 Downside): This is the big one. When you buy an annuity, you are giving up access to that lump sum of money. That money is “locked up” in exchange for the guarantee of lifelong income.

- Inflation: The paycheck is fixed. A $700 check is great today, but its buying power will be less in 20 years.

- Fees (Surrender Charges): If you try to pull your money out early (usually in the first 5-7 years), you will pay a massive “surrender charge.” An annuity is a long-term commitment.

Annuity vs. CD: Which Tool is for Which Job?

This is the most common question seniors ask, and it’s the most important one to get right. Both CDs and Fixed Annuities are “safe money” tools, but they have completely different jobs.

Choosing the wrong one for your goal can be a major financial mistake. Let’s break it down.

Tool #1: A CD (Certificate of Deposit)

- What is its “Job”?

A CD is a short-term savings tool. Its job is to protect your lump sum of money for a fixed, short period (usually 1 to 5 years) while it earns a guaranteed fixed interest rate. It’s a “waiting room” for your money. - The Honest Pros:

- 100% Safe: CDs are FDIC-insured up to $250,000. This is the highest level of safety you can get, backed by the U.S. government.

- Simple: They are easy to understand. There are no hidden fees.

- Liquidity: You always get your full principal back, plus interest, at the end of the term (e.g., in 2 years).

- The Honest Cons:

- It Does NOT Solve Your #1 Fear: A CD does not, and cannot, guarantee you a lifelong income. When it matures, you get your money back, and you are right back in the same position: worried about that money running out.

- Low Returns: The interest rates on CDs are often very low, sometimes not even keeping up with inflation.

Bottom Line: A CD is the perfect tool for an emergency fund or for money you know you’ll need for a specific, near-future purchase (like a new car or a 5-year roof repair).

Tool #2: A Fixed Annuity (Our Recommendation for Income)

- What is its “Job”?

A Fixed Annuity is a long-term income tool. Its job is to turn your lump sum of savings into a guaranteed, lifelong monthly paycheck. It’s a “paycheck factory.” - The Honest Pros:

- It Solves Your #1 Fear: This is its superpower. It is the only tool that can give you a 100% guarantee that you cannot outlive your income.

- Safe from Market Risk: A fixed annuity is not in the stock market. You are guaranteed a fixed, predictable check no matter what happens on Wall Street.

- The Honest Cons (The Trade-Offs):

- It is NOT FDIC-Insured: This is a critical difference. It is backed by the insurance company itself. This is why you must choose a top-rated, “A” or “A++” strength company.

- Very Low Liquidity: This is the big trade-off. You must be 100% comfortable with this. You are giving the insurance company your lump sum in exchange for the guarantee of lifelong payments. You cannot call them and ask for your $100,000 back. That money is gone; it has been converted into an income stream.

Bottom Line: An annuity is the perfect tool for your core retirement funds—the money you absolutely must have to pay your mortgage, rent, and monthly bills for the rest of your life.

At-a-Glance: The "Job" Comparison

|

Feature

|

A CD (Certificate of Deposit)

|

A Fixed Annuity

|

|---|---|---|

|

Main "Job"

|

Short-Term Savings (Protecting your lump sum)

|

Long-Term Income (Creating a paycheck for life)

|

|

How You Get Paid

|

You get your full principal + interest back at the end (e.g., in 2 years).

|

You get a monthly paycheck, but you give up the lump sum.

|

|

Liquidity

|

High. You know you'll get your money back on a set date.

|

Very Low. Your money is "locked up" to fund the guarantee.

|

|

Safety

|

Extremely High. Backed by the FDIC (government).

|

High (but different). Backed by the insurance company and state guaranty funds.

|

|

Problem it Solves

|

Protects your money from being spent for 1-5 years.

|

Solves the fear of outliving your money.

|

|

Best For...

|

An Emergency Fund or money you'll need for a specific purchase.

|

Your "must-have" income (e.g., money to pay your rent/mortgage for life).

|

Frequently Asked Questions (FAQ)

This is the #1 fear. “What if I put in $100,000 and die a year later?” You have options to prevent this. You can add a “Period Certain” feature, which guarantees the policy will pay out for at least 10 or 20 years. If you die in year 5, your beneficiary (your child) will keep getting the checks for the remaining 15 years.

This is a very smart question. Your annuity is a contract with the insurance company, so you must choose a highly-rated, “A” or “A++” strength company. Furthermore, every state has a State Guaranty Association that protects your policy (up to a certain limit) if the insurer were to fail.

This is a high fee (e.g., 7%) that you will pay if you try to withdraw your money during the “surrender period” (usually the first 5-7 years of the contract). An annuity is a commitment. You should not put any money into it that you might need for an emergency.

This is the “surrender charge” in practice. Most policies will let you withdraw a small amount (like 10%) each year without a fee, but taking out large amounts will trigger that high surrender charge.

This is the most important question. A simple, fixed annuity is not an investment—it is insurance. You are not trying to “beat the market” or get rich. You are insuring yourself against the risk of running out of money. It is a tool for guaranteed safety, not for risky growth.