If you are retired today — or helping a parent plan for retirement — your biggest threat isn’t market volatility. It’s the silent Invisible Thief called inflation.

Your “fixed income” may look steady on paper, but the real cost of groceries, utilities, prescription drugs, and healthcare keeps rising. In the last few years alone, many seniors have seen their purchasing power shrink by 15% or more.

A standard fixed annuity that paid $2,000 per month five years ago now feels noticeably smaller at the grocery store or pharmacy. This is the Purchasing Power Trap — and it only gets worse over time.

At Sagewise, we help families protect their retirement with a clear Sagewise Audit of inflation-fighting tools: Inflation-Protected Annuities and COLA Riders. In this guide, we break down the real math, the trade-offs, and practical strategies that make sense for seniors and their families in 2026.

Key Takeaways

- A fixed $2,000 monthly payment today could lose nearly half its real value by age 85 at average inflation rates.

- COLA Riders automatically increase your annuity payment by 1–3% each year.

- The main trade-off: Adding a COLA rider typically reduces your starting monthly payment by 25–30%.

- The break-even point usually occurs between 10–14 years — after that, the growing payment pulls ahead.

- An Annuity Ladder strategy offers a smart middle-ground solution without the large initial cut.

Don’t let inflation quietly erode the comfortable retirement you (or your loved ones) have earned.

Get Your Free, Personalized Annuity Quote Protect your purchasing power today →

The sageWISE Audit: Understanding the “Purchasing Power” Math

While the official Consumer Price Index (CPI-U) tracks general inflation, seniors often face the CPI-E (Elderly Index), which weighs healthcare, housing, and transportation more heavily — and typically runs a bit higher.

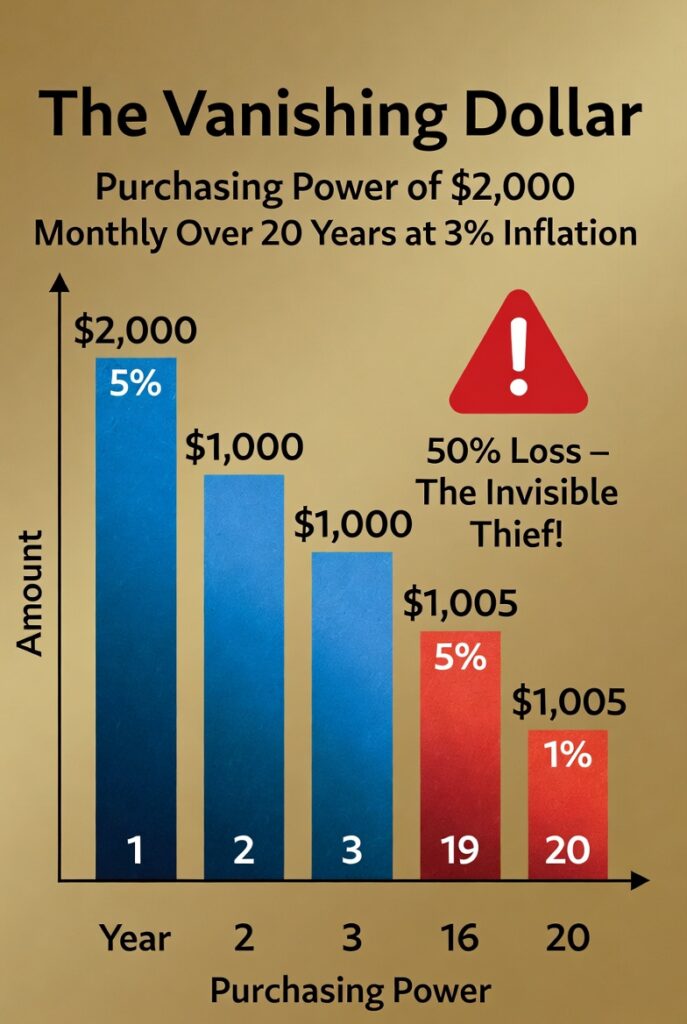

The 20-Year Erosion Test

Here’s what happens to a $2,000 monthly fixed annuity payment at a conservative 3% average annual inflation rate:

|

Year

|

Monthly Check (Nominal)

|

Real Purchasing Power (Today’s Dollars)

|

% Loss from Original

|

|---|---|---|---|

|

Year 1

|

$2,000

|

$2,000

|

0%

|

|

Year 5

|

$2,000

|

$1,684

|

-16%

|

|

Year 10

|

$2,000

|

$1,418

|

-29%

|

|

Year 15

|

$2,000

|

$1,194

|

-40%

|

|

Year 20

|

$2,000

|

$1,005

|

-50%

|

Verdict: Without protection, a standard fixed annuity can lose half its buying power by your mid-80s. This is why many families later face difficult choices around debt or tapping home equity.

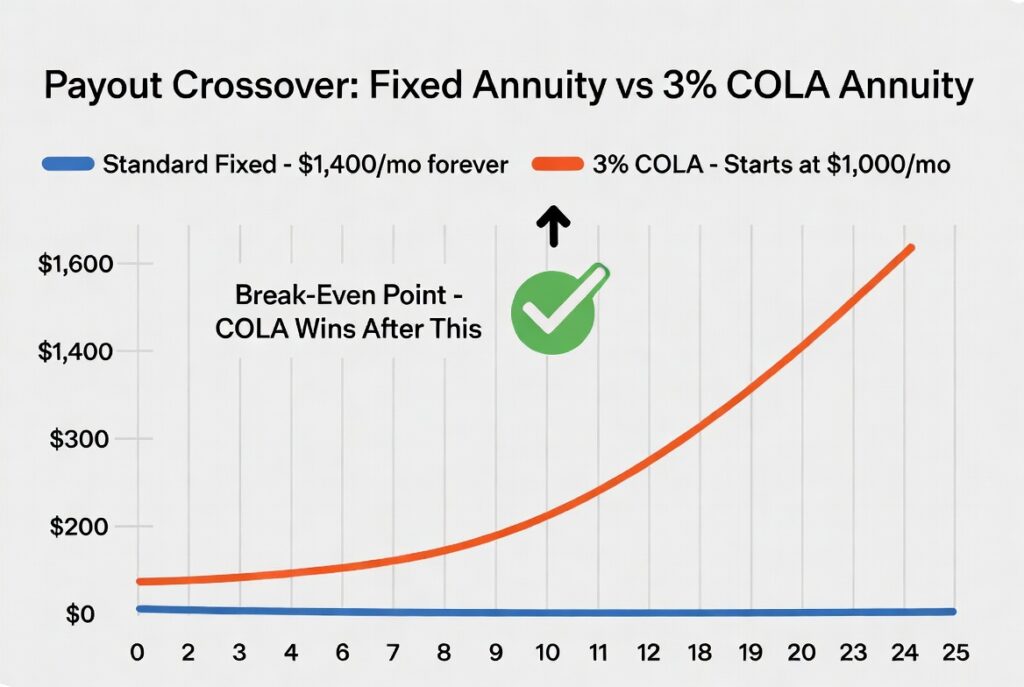

Strategy #1: The COLA (Cost-of-Living Adjustment) Rider

A COLA rider is the most straightforward way to add inflation protection directly inside your annuity. It guarantees your monthly check will increase by a fixed percentage (usually 1%, 2%, or 3%) every year on your contract anniversary — and the increases compound over time.

Real-World Example (3% COLA Rider):

- Year 1: $1,000

- Year 2: $1,030

- Year 10: ~$1,344

- Year 20: ~$1,806

The Trade-Off Table

|

Annuity Option

|

Starting Monthly Payment

|

Year 10 Payment

|

Year 20 Payment

|

Best Suited For

|

|---|---|---|---|---|

|

Standard Fixed Annuity

|

$1,400

|

$1,400

|

$1,400

|

Shorter life expectancy or maximum income now

|

|

3% COLA Rider Annuity

|

$1,000

|

$1,344

|

$1,806

|

Excellent health and longevity (living past 85)

|

Pro Tip: If you or your parent are in very good health and expect a long retirement, the COLA rider often wins in the long run. If health is a concern, the higher starting fixed payment may be more practical.

Try our free tool: See exactly how different COLA options affect your payout → Annuity Payout Estimator

Strategy #2: CPI-U Linked Annuities

These rare “inflation-indexed” annuities adjust your payment directly based on the official CPI-U. If inflation jumps to 6–8%, your check rises accordingly.

Advantages: Closest thing to true inflation protection.

Drawbacks: Very few carriers still offer them, and they are more expensive (lower starting payout). Most now use fixed-percentage COLA riders instead.

Sagewise Recommendation in 2026: A strong 2–3% COLA rider combined with an Annuity Ladder strategy is usually the most realistic and effective solution for most families.

Do You Need Inflation Protection? – Quick Checklist

Answer these questions honestly:

- Social Security is my (or my parent’s) only other reliable income source.

- I am purchasing this annuity before age 70 (long time horizon).

- I’m concerned about future assisted living or home care costs.

- I do not have a large stock or real estate portfolio acting as a natural inflation hedge.

If you checked 2 or more boxes → You should strongly consider inflation protection.

Smart Alternative: The Annuity Ladder Strategy

Instead of buying one large annuity with a COLA rider, many families build an Annuity Ladder — purchasing smaller fixed annuities every few years.

Example Ladder:

- Age 65: Buy a $100,000 fixed annuity

- Age 70: Buy another $100,000 fixed annuity (often at a higher payout rate)

- Age 75: Buy a third $100,000 fixed annuity

Benefits:

- Avoids the 25–30% reduction in starting income from a COLA rider

- Naturally steps up income over time

- Preserves more liquidity in early retirement years

FAQ: Inflation-Protected Annuities & COLA Riders

A COLA (Cost-of-Living Adjustment) rider is an optional feature that automatically increases your monthly annuity payment by a fixed percentage (typically 1%, 2%, or 3%) each year. This helps your income keep pace with rising prices so your purchasing power doesn’t shrink over time.

Not as an upfront fee. Instead, the insurance company reduces your starting monthly payment (usually by 25–30%) to fund the future increases. It’s a trade-off: lower income now for growing income later.

Most people reach the break-even point between 10 and 14 years. After that, the COLA version typically pays more for the rest of your life. This makes it especially valuable if you or your loved one expect a long retirement (past age 85).

CPI-linked annuities can provide closer tracking to actual inflation, but they are rare in 2026 and usually more expensive. Fixed-percentage COLA riders (2–3%) are more widely available and offer predictable, guaranteed growth.

Yes — healthcare and assisted living costs often rise faster than general inflation. A COLA rider or Annuity Ladder can help ensure you have more income available when these expenses increase.

It depends on your situation. An Annuity Ladder avoids the big initial payout cut and lets you take advantage of future interest rates and your increasing age (which usually means higher payouts). Many families combine both strategies for balanced protection.

No — once chosen, the rider is part of the contract. That’s why it’s important to run personalized numbers and understand your health and life expectancy before deciding.

Yes. The increases are contractually guaranteed by the insurance company (backed by state guaranty associations, with limits varying by state). Your income will rise as promised regardless of market conditions.

In 2026, rates remain attractive for fixed annuities. Waiting means more years of inflation eroding your savings and missing out on locking in today’s guaranteed income.

It depends on age, health, other income sources (like Social Security), and how long you expect to need the income. Our free tools and advisors can run side-by-side comparisons tailored to your situation.

Ready to Protect Your Retirement?

Inflation doesn’t have to steal the lifestyle you’ve worked so hard for. Whether you choose a COLA rider, a CPI-linked annuity (when available), or a well-planned Annuity Ladder, the most important step is getting clear numbers tailored to your situation.

👉 Get Your Free, Personalized Annuity Quote

Secure a growing paycheck that lasts as long as you do →

Our licensed advisors will compare top-rated carriers and show you clear side-by-side illustrations with no pressure.

Try our free tool first: Annuity Payout Estimator

This article is for educational purposes only. Annuity guarantees are backed by the financial strength of the issuing insurance company. Always review the contract and consult with a qualified financial professional.