You’ve seen the mailers. You’ve heard the radio ads. You may have even sat through a “free steak dinner” seminar where a charismatic advisor promised you a “Guaranteed 7% Return” regardless of what happens in the stock market.

In a world of 1% savings accounts and volatile index funds, 7% sounds like a miracle. It sounds like the ultimate “Financial Bodyguard” for your retirement.

But here is the sageWISE Warning: In the world of annuities, 7% growth is almost never “real money” that you can walk away with. It is a psychological math trick used to anchor you to a specific insurance company for life.

As your trusted advocate, we have performed an exhaustive audit of Guaranteed Lifetime Withdrawal Benefits (GLWB) and Income Riders. We will show you the difference between your “Account Value” and your “Benefit Base,” explain why a high roll-up rate often leads to a lower withdrawal percentage, and provide the exact math you need to see if your “7% guarantee” is actually a high-cost cage.

Key Takeaways

- The Great Divide: Your annuity has two values. The Account Value is the cash you actually own. The Benefit Base is “Monopoly Money” used solely to calculate your future paycheck.

- The Roll-up Rate: That 7% or 8% guarantee only applies to the Benefit Base. If you cancel the policy, you don’t get that 7%—you only get the (often lower) market return of the Account Value.

- The Fee Friction: Income riders typically cost 1.00% to 1.50% per year. This fee is usually deducted from your real cash Account Value, even if the market is down.

- The Withdrawal Trap: A company might offer a high 7% growth rate but only allow a 4% withdrawal rate. Another company might offer 0% growth but a 6% withdrawal rate. The second company often pays a higher check.

Don’t be fooled by “Monopoly Money.” See if your annuity income is actually optimized for 2026.

Get Your Free, Personalized Annuity Quote

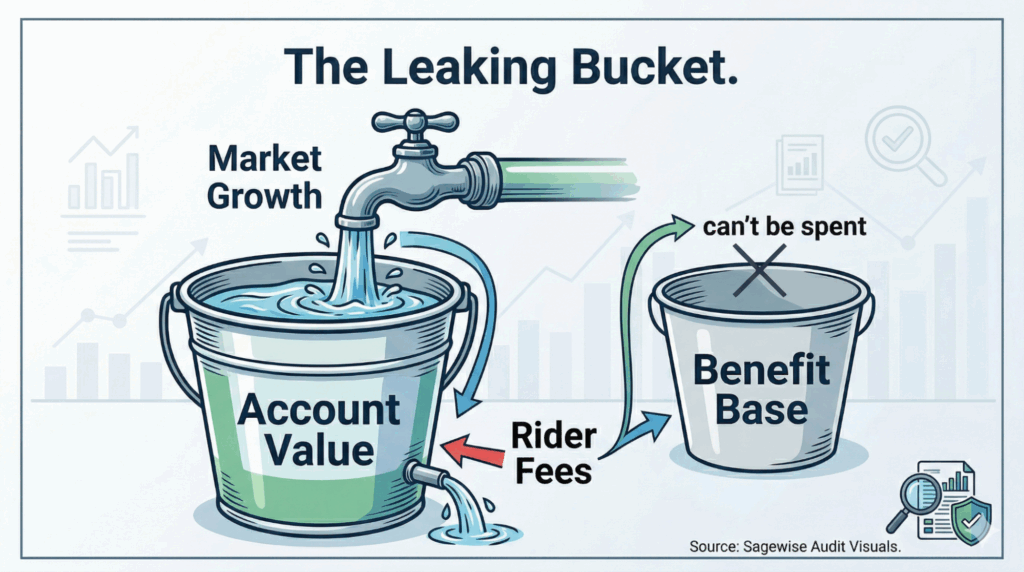

The sageWISE Audit: "Real Cash" vs. "Benefit Base"

To be your own financial bodyguard, you must understand that when you buy an annuity with an income rider, you are essentially managing two different bank accounts that never touch.

Account 1: The Account Value (Your Real Cash)

This is the “Walk-Away” value. If you decide you want to cancel your annuity and go buy a boat or a Gold IRA, this is the money you get (minus any surrender charges). It grows based on the interest rate of the fixed annuity or the performance of the Index-Linked options.

Account 2: The Benefit Base (The Income Anchor)

This is a ledger entry. If the brochure says “7% Compound Growth,” this is the account that is growing.

- The Catch: You can NEVER withdraw this as a lump sum.

- The Purpose: The insurance company says, “We will pretend you have this much money when we calculate your lifetime paycheck.”

Scenario: The $200,000 Deposit Imagine you deposit $200,000 into an annuity with a 7% Income Rider. After 10 years, the math looks like this:

|

Feature

|

Account Value (Real Cash)

|

Benefit Base (Income Math)

|

|---|---|---|

|

Initial Deposit

|

$200,000

|

$200,000

|

|

Growth Strategy

|

S&P 500 Index (5% Avg)

|

7% Guaranteed Roll-up

|

|

Value After 10 Years

|

**~$325,000**

|

~$393,000

|

The Moment of Truth: If you want to move your money to a different company, you get $325,000. The $393,000 simply “vanishes” because it was never your money—it was a calculation tool.

The "Withdrawal Percentage" Shell Game

This is where the psychological trick becomes a financial burden. Seniors are often so focused on the 7% growth that they forget to look at the Withdrawal Percentage.

Insurance companies use a formula:

Annual Check = Benefit Base x Withdrawal Percentage

The Comparison Audit:

- Company A (The “Marketing Giant”): Offers a 7% Roll-up but only a 4% Withdrawal Rate for a 65-year-old.

- Company B (The “Low Key Auditor”): Offers a 0% Roll-up but a 6% Withdrawal Rate for a 65-year-old.

The Result (10 years later on a $100k deposit):

- Company A: $196,715 (Benefit Base) x 4% = **$7,868 / year**.

- Company B: $100,000 (Benefit Base) x 6% = **$6,000 / year**.

Wait, Company A pays more? Yes—BUT only if you wait 10 years to start. If you started the income immediately, Company B would pay $6,000 while Company A only pays $4,000.

The sageWISE Warning: Companies with high “guaranteed growth” percentages often have the highest fees and the lowest starting withdrawal rates. They are betting that you will get “anchored” to that high Benefit Base and never leave, even if a 1035 Exchange to a simpler product would result in a higher check.

The "Fee Friction" Trap

Income riders are not free. They typically cost between 1.10% and 1.50% per year.

The Double-Dipping Fee: Most companies charge the 1.25% fee based on the Benefit Base, not the Account Value.

- The Math of Destruction: If your real cash is $100k but your Benefit Base is $200k, a 1.25% fee is actually **$2,500**. That is a 2.5% fee on the money you actually own.

- The Result: Over 20 years, these fees can cannibalize your real cash, making it impossible for you to ever leave the contract without taking a massive loss. This is why we call it the “Annuity Cage.”

The Income Rider Checklist

Before you sign an annuity contract with an “Income Rider,” ask your advisor these five specific questions. If they can’t (or won’t) answer them in writing, walk away.

- [ ] What is the fee? (Is it charged on the Account Value or the Benefit Base?)

- [ ] Can I ever walk away with the “Guaranteed” amount? (The answer will be ‘No,’ but listen to how they explain it.)

- [ ] What is the “Payout Factor” at age 65, 70, and 75? (Compare this to a simple Single Premium Immediate Annuity (SPIA).)

- [ ] Is the growth “Simple” or “Compound”? (7% simple growth is significantly less than 7% compound growth over 10 years.)

- [ ] Does the rider stop if the Account Value hits zero? (A true “Financial Bodyguard” rider continues to pay even after the cash is gone.)

Strategic Alternative: The "Pure" Income Play

As your advocate, we often find that seniors are better off skipping the “Income Rider” and its 1.25% fee.

The Strategy: Instead of paying for a complex rider, put your money into a high-quality Fixed Index Annuity (FIA) with no rider fees. When you are ready for income, simply “Annuitize” the contract or use a 1035 exchange to move the (now larger) cash balance into a SPIA.

The Benefit: You save 1.25% in fees every single year. Over 10 years, that is 12.5% more principal that stays in your pocket. You maintain your Liquidity and keep your options open to invest in Gold or Real Estate later.

FAQ: Common Income Rider Myths

Generally, no. The “Roll-up” usually stops the moment you take your first dollar. At that point, the Benefit Base is locked, and your check is fixed for life.

Some riders have a “Nursing Home Doubler” where your income check doubles if you go into a facility. However, this is usually just the company paying you your own money faster. It is not a gift from the insurer.

No. Upon death, the Benefit Base usually vanishes. Your heirs only receive the Account Value (the real cash). If you want to leave a legacy, an income rider is often the worst way to do it. See our guide on Annuity Death Benefits for better options.

Only when you receive it as income. Because the 7% isn’t “real money” until it’s paid out, you don’t pay taxes on the growth of the Benefit Base. However, the income checks themselves will be taxed based on the Exclusion Ratio.

Because of Anxiety. The insurance company is selling “Certainty.” For a senior who is terrified of running out of money, a “Guaranteed 7%” sounds like safety. Our job is to show you that you can achieve that same safety with lower fees and more control.

Get Your Free Annuity Quote (Audit your income strategy. Secure your real cash today.)