When you turn on the television, you are bombarded with millions of dollars in advertising from the “Big Four” insurance giants. They use catchy jingles, funny mascots, and celebrity spokespeople to build a single message: Trust us, we are the only name you need to know.

For decades, many seniors have followed this marketing, staying with the same “Captive” agent for 20 or 30 years. You assume that because you have a personal relationship with the agent at the local State Farm or Allstate office, they are shopping the market to get you the best deal.

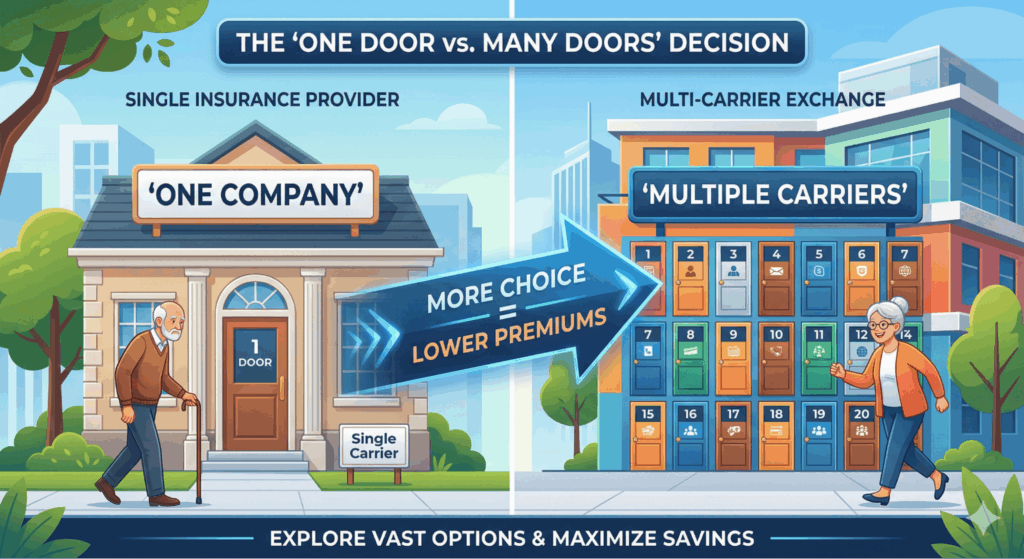

But here is the sageWISE Warning: A “Captive” agent is legally a salesperson for one company. They cannot show you a lower rate from a competitor, even if they know you are being overcharged.

To truly protect your retirement budget, you need a Financial Bodyguard who has access to the entire market, not just one brand’s price list. This is where the Independent Broker comes in. In 2026, the price difference between a big-box carrier and a specialized “Senior-Preferred” carrier can be $400 to $800 per year. If you aren’t using an independent broker, you aren’t shopping; you are just being sold.

As your trusted advocate, we have performed a Sagewise Audit of the insurance distribution system. We will show you the “One-Quote Trap,” explain how brokers find “Hidden” senior carriers, and provide the exact checklist to vet your next insurance partner.

Key Takeaways

- Captive vs. Independent: Captive agents work for the bank; Independent brokers work for YOU.

- Market Access: An independent broker can check 20+ companies with one phone call, while a captive agent can only check one.

- The “Non-Standard” Advantage: Brokers have access to regional carriers that specialize in seniors and offer lower rates for low-mileage drivers.

- Claims Advocacy: Because brokers aren’t employees of the insurance company, they can act as your advocate during a difficult claims process.

Stop being a “customer” and start being a “client.” See if a broker can find a better rate for your profile.

Check Your New Senior Rate Now

The sageWISE Audit: "Captive" vs. "Independent"

To understand why you might be overpaying, you must understand who your agent actually works for.

1. The Captive Agent (The Company Salesman)

Companies like State Farm, GEICO, Allstate, and Farmers use captive agents. These agents are either employees or exclusive contractors.

- The Conflict: Their contract prevents them from selling any other brand. If their company raises your rates by 20%, their only choice is to try and lower your coverage (which puts your assets at risk) or hope you don’t notice the Loyalty Tax.

- The “Service” Illusion: They may be very friendly and active in your community, but their hands are tied by corporate pricing algorithms.

2. The Independent Broker (The Market Auditor)

Independent brokers (like those at Trusted Choice agencies) do not work for one company. They hold “appointments” with dozens of carriers like Travelers, Safeco, Progressive, Hartford, and Cincinnati Insurance.

- The Advantage: They are “Aggregators.” When your rate goes up, they simply move you to a different company in their system. They don’t lose you as a client; they just change the logo on your policy.

- The Objective Truth: Because they aren’t married to one brand, they can tell you the truth: “Company A is currently overpriced for seniors in our zip code, let’s move you to Company B.”

3 Ways Independent Brokers Find "Senior Gold"

Why is the “Broker Edge” so sharp for retirees? It comes down to Risk Niches. Insurance companies change their “Appetite” for different groups of people every few months.

A. The "Regional" Advantage

Big-name companies have massive national overhead. Local or regional carriers (like Auto-Owners or Erie) often have lower overhead and focus specifically on stable, low-risk demographics—like retired homeowners. These companies often don’t advertise on TV, so you can’t find them without a broker.

B. Accurate Mileage Rating

As we noted in our Low-Mileage Hack guide, driving under 5,000 miles can slash your premium. Big-box carriers often use “Default” mileage tiers (e.g., 10,000 miles) that are hard to change. Independent brokers work with carriers that have “Pay-Per-Mile” or specific “Retired/Pleasure” tiers that are much more flexible.

C. The "Non-Standard" Recovery

If you’ve had a minor accident or a lapse in coverage, big-name companies will often move you to their “Non-Standard” (High Risk) tier and leave you there for 5 years. A broker can shop the “Mid-Market” carriers who are willing to forgive a single “senior moment” much faster, saving you thousands in surcharges.

Side-by-Side: The Senior Shopping Experience

|

Feature

|

Captive Agent (State Farm/Allstate)

|

Independent Broker

|

|---|---|---|

|

Brands Offered

|

Only One

|

10 to 50+

|

|

Loyalty Reward

|

Usually a small discount.

|

Shopping the market every 3 years.

|

|

If Rates Rise?

|

You have to leave the agent.

|

The agent finds you a new brand.

|

|

Policy Review

|

Focuses on cross-selling.

|

Focuses on Price Benchmarking.

|

|

Verdict

|

Best for "Simplicity"

|

Best for "Value Protection"

|

The "Claims Bodyguard" Factor

This is the most overlooked benefit of the independent path. When you have a wreck and file a Diminished Value claim, you are essentially in a legal dispute with the insurance company.

- The Captive Problem: If you complain to a captive agent about a slow claim, they are complaining to their own boss. They have limited leverage.

The Broker Solution: If an insurance company treats a broker’s client poorly, that broker can threaten to move all their clients to a competitor. This “Portfolio Leverage” often results in faster claim processing and fairer settlements for the senior.

Step-by-Step: How to Find Your Financial Bodyguard

Don’t just pick a name from the phone book. Follow this roadmap to find a broker who understands the needs of a retiree.

Step 1: Use the "Senior Driver Discount Finder"

Before you even talk to a broker, know what you are entitled to. Use our Senior Driver Discount Finder to identify if you qualify for defensive driving or low-mileage credits. Take this data to the broker and ask: “Which of your carriers gives the biggest credit for these?”

Step 2: Check for "A" Ratings

A low price is useless if the company goes bust. Ask the broker for the A.M. Best Rating of every carrier they suggest. At Sagewise, we only recommend carriers with an A- (Excellent) rating or higher.

Step 3: The "Three-Year Audit" Commitment

Ask the broker: “Will you automatically re-shop my policy if my rate increases by more than 10%?” A true advocate will offer a “Renewal Review” as part of their standard service to prevent you from ever paying a Loyalty Tax again.

Frequently Asked Questions (FAQ)

No. This is the biggest myth. Brokers are paid a commission by the insurance company, just like captive agents. The “Retail” price of the policy is the same whether you buy it yourself or through a broker. In fact, because they have more choices, they are almost always cheaper.

Yes, and they are better at it. As we noted in our Snowbird Guide, insuring cars in two states is complex. An independent broker can often hold licenses in multiple states, allowing them to manage your northern and southern policies through one point of contact.

Absolutely. As we warned in our Adding a Grandchild guide, this can triple your rates. Brokers specialize in finding the “Standard” carriers that are the least punitive toward multi-generational households.

Independent brokers are the kings of the “Smart Bundle.” They can find one company to cover both, or—even better—they can find two different companies that offer a “Companion Discount.” This gives you the savings of a bundle with the customized coverage of a standalone policy.

Look at their business card or website. If it only has one logo (like the big red State Farm logo), they are captive. If it has their own name (e.g., “Smith & Associates Insurance”) and lists multiple company logos at the bottom, they are independent.

Check Your New Senior Rate Now (Stop paying for marketing. Start paying for protection today.)