In retirement, your financial strategy shifts from “accumulation” to “preservation.” You are likely living on a fixed income, which means inflation is your biggest enemy. Every time the price of eggs or gas goes up, your purchasing power goes down.

The right credit card isn’t about racking up debt; it’s about fighting back.

Smart seniors use credit cards as “discount tools.” By using a card that offers 3-5% cash back on your essential daily spending, you are effectively giving yourself a permanent discount on life, keeping more money in your pocket for the things you enjoy.

As your trusted advocate, we have selected the top 5 cards that offer simplicity (no annual fees) and high rewards on the categories that matter most to seniors: groceries, gas, and healthcare.

Key Takeaways

- Rule #1: No Annual Fees. You should never pay a fee to use a credit card. All the cards on this list are free to hold.

- Beat Inflation: Look for cards that offer 3% to 5% cash back on groceries and gas—these are your highest variable costs.

- Simplicity Wins: If you hate tracking categories, a flat-rate 2% cash back card is your best friend.

- Medical Rewards: Some cards now specialize in cash back for drugstores and medical expenses, a huge benefit for seniors.

The 5 Best Cash Back Cards for Seniors at a Glance

We rated these cards based on their ability to put cash back in your pocket without charging you an annual fee.

|

Card Name

|

Sagewise Rating

|

Best For

|

Key Benefit

|

|---|---|---|---|

|

Blue Cash Everyday® (Amex)

|

5.0 / 5.0

|

Groceries & Gas

|

3% Cash Back at U.S. supermarkets, gas stations, and online retail.

|

|

Citi Double Cash®

|

5.0 / 5.0

|

Simplicity (Flat Rate)

|

Earn 2% on everything (1% when you buy, 1% when you pay).

|

|

Chase Freedom Unlimited®

|

4.5 / 5.0

|

Drugstores & Dining

|

3% Cash Back on dining and drugstores (essential for seniors).

|

|

Capital One Quicksilver

|

4.0 / 5.0

|

Travel & Simplicity

|

1.5% on everything with No Foreign Transaction Fees.

|

|

AARP® Essential Rewards

|

4.0 / 5.0

|

Medical Expenses

|

3% Cash Back on gas and drugstores; 2% on medical expenses.

|

hi gchgcgh

Security Alert: Essential Features for Seniors

Seniors are frequently targeted by scammers. The credit card you choose should be your first line of defense. All the cards on our list include these three non-negotiable safety features:

- $0 Fraud Liability: If your card is lost, stolen, or used online without your permission, you are legally not responsible for a single penny of the unauthorized charges.

- Instant Transaction Alerts: You can set up the card to send a text message to your phone immediately every time a purchase is made. This is the fastest way to spot a thief.

- US-Based Customer Support: When there is a problem, you need to be able to hear and understand the person helping you. Premium cards (like Discover and Amex) are famous for their clear, helpful support teams.

The ‘Inflation Offset’ Strategy: How to Pay One Bill for Free

Don’t just let your cash back sit there. Use it strategically to “erase” inflation from your budget.

The Scenario: You spend $500/month on groceries and $150/month on gas.

- Using Cash/Debit: You get $0 back.

- Using the Amex Blue Cash Everyday: You earn 3% back ($19.50/month).

The Result: Over a year, that is $234 in free money. That is enough to pay for two months of your electric bill or cover your entire Netflix subscription for the year. By simply changing how you pay, you have given yourself a raise.

Which Spender Are You? Finding Your Perfect Match

Still not sure? Find your “Spender Personality” below to see which card fits your lifestyle.

|

If you are...

|

Your Goal Is...

|

The Best Card Is...

|

|---|---|---|

|

The Home Chef

|

Saving on weekly grocery runs and gas fill-ups.

|

Amex Blue Cash Everyday

|

|

The "Set it and Forget it"

|

Getting a good deal without tracking categories.

|

Citi Double Cash

|

|

The Socializer

|

Dining out with friends and picking up prescriptions.

|

Chase Freedom Unlimited

|

|

The Snowbird/Traveler

|

Avoiding fees while traveling or cruising abroad.

|

Capital One Quicksilver

|

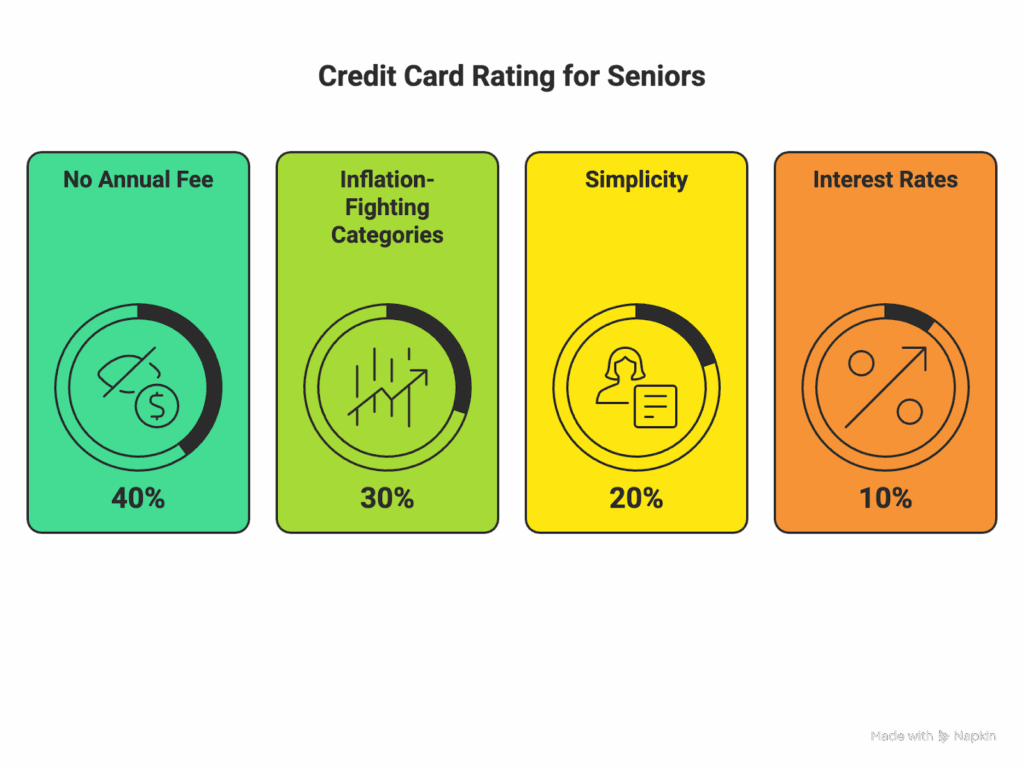

How We Rate Credit Cards for Seniors

At Sagewise, we ignore the “flashy” perks like airport lounges or travel points that require complex transfers. We focus on the financial reality of a fixed income. We weigh these factors:

- No Annual Fee (40%): We believe seniors should not pay for the privilege of using a credit card. All our top picks are free to hold.

- Inflation-Fighting Categories (30%): We prioritize cards that give high cash back (3%+) on necessities like food, gas, and medicine.

- Simplicity (20%): We favor cards with easy redemption processes (cash or statement credits) over complex point systems.

- Interest Rates (10%): While we advise paying in full, we look for cards that offer competitive APRs or 0% introductory periods for emergencies.

Your 'Wallet Audit' Checklist

Do you have the right tools in your wallet? Use this checklist to see if you are maximizing your discounts.

- [ ] 1. Do I have a “Grocery” card?

- Goal: You should be earning at least 3% back on every supermarket trip. (Recommendation: Amex Blue Cash Everyday)

- [ ] 2. Do I have a “Pharmacy” card?

- Goal: If you spend more than $100/month at the drugstore, you should be earning 3% back. (Recommendation: Chase Freedom Unlimited)

- [ ] 3. Do I have a “Catch-All” card?

- Goal: For everything else (utilities, insurance premiums, clothes), you should earn a flat 2%. (Recommendation: Citi Double Cash)

- [ ] 4. Am I paying an Annual Fee?

- Action: If you are paying $95+ a year for a card you rarely use for travel perks, cancel or downgrade it to a no-fee version immediately.

Frequently Asked Questions (FAQ)

Yes, slightly and temporarily. When you apply, the bank does a “hard pull” on your credit, which may drop your score by 5-10 points. However, if you pay on time and keep your balance low, your score will typically recover quickly and may even increase due to having more available credit.

No. If you carry a balance, the interest rate (often 20%+) will completely wipe out any 2% or 3% cash back you earn. If you have debt, ignore rewards and focus on finding a Low Interest or

It’s very simple. Most banks allow you to apply your cash back as a “Statement Credit.” This means they simply reduce your monthly bill by the amount of cash you earned. It’s the easiest way to save.

Some do. The Capital One Quicksilver is the only one on this list that explicitly has No Foreign Transaction Fees. If you travel internationally, use that card to avoid the extra 3% charge.

Yes! The smartest strategy is to pair them. Use the Amex for groceries and gas, the Chase card for dining and pharmacy, and the Citi card for everything else. This ensures you are getting the maximum discount on every single purchase.