When you take out a Home Equity Line of Credit (HELOC), the bank effectively becomes a “silent partner” in your home. While this is a powerful tool to access cash for medical bills or necessary repairs, it creates a significant question for your legacy: What happens to that debt when you pass away?

Many seniors worry that their children will be personally liable for the balance, or worse, that the bank will “seize” the house the moment they are gone. The reality is that while your heirs do not personally inherit the debt, the home does. When you pass away, the HELOC balance remains attached to the property as a legal lien. Your heirs are not required to pay the bank out of their own pockets, but the bank must be satisfied before the title of the home can be legally transferred to your children or sold.

As your trusted advocate, we are here to act as your financial bodyguard. We will break down the “Due-on-Sale” clause, compare the three paths your heirs can take, and show you how to use life insurance to “zero out” the debt automatically.

Key Takeaways

- Lien vs. Liability: Your children aren’t personally responsible for the cash, but the bank holds a claim against the home’s value.

- The “Due on Sale” Clause: Most HELOC contracts require the full balance to be paid immediately if the home is sold or ownership is transferred.

- The Death Freeze: Banks often freeze the line of credit the moment they are notified of a death, stopping any further “draws” by a spouse or executor.

- The Strategy: Matching your HELOC balance with a Final Expense Policy ensures the home stays in the family debt-free.

Protect your legacy and your family’s future. Lower your monthly costs safely.

Explore Debt Relief Options

The "Death Freeze": Why Access Stops Instantly

One of the most stressful moments for a surviving spouse or child is discovering the “HELOC Freeze.” In many contracts, the bank includes a clause that allows them to suspend the draw period upon the death of a primary borrower.

- The Scenario: You and your spouse have a $50,000 HELOC. You pass away. Your spouse tries to draw $5,000 for funeral costs.

- The Reality: The bank sees the death certificate and locks the account. Even if there is $40,000 in available credit, that “ATM” is now closed.

- The Bodyguard Tip: Ensure your spouse is a Co-Borrower, not just an “Authorized User.” Under the Consumer Financial Protection Bureau (CFPB) rules, a co-borrower often has more protections to maintain the account during the transition.

The 3 Choices Your Heirs Must Make

When the estate is settled, your heirs will be presented with three specific paths. Use this table to understand the pros and cons of each.

|

Choice

|

How it Works

|

Best For...

|

|---|---|---|

|

1. Sell the Home

|

Heirs sell the house, pay the bank from the proceeds, and keep the leftover cash.

|

Heirs who don't want to live in or manage the property.

|

|

2. Refinance

|

Heirs take out a new mortgage in their own name to pay off your HELOC.

|

Heirs who want to keep the home but don't have $20,000+ in cash.

|

|

3. Pay in Cash

|

Heirs use a Life Insurance payout or savings to clear the lien.

|

The "Gold Standard." Keeps the home in the family debt-free instantly.

|

1. Selling the Property

This is the most common path. If you owe $30,000 on a HELOC and the home sells for $400,000, the bank takes their $30,000 at the closing table, and your children receive a check for $370,000.

2. Refinancing into Their Own Name

If your daughter wants to move into your home, she must satisfy the “Due-on-Sale” clause. Since she likely doesn’t have the cash to pay the bank, she can apply for her own mortgage. The new loan pays off your HELOC, and the home is transferred to her name.

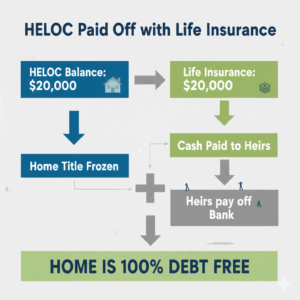

3. The Life Insurance “Sweep” Strategy

This is how savvy seniors ensure their home stays in the family without a stressful legal battle. You purchase a small, permanent life insurance policy that mirrors your HELOC balance.

The Debt-Free Legacy Flow

The "Due-on-Sale" Clause: A Technical Warning

Most HELOCs are “non-assumable.” This means your children cannot simply “take over” your 8% interest rate and keep making your $200 monthly payments.

Under federal law (the Garn-St. Germain Act), banks are generally prohibited from triggering this clause when a home is left to a relative. However, this protection usually applies to the Primary Mortgage, not necessarily the HELOC. Many lenders will still demand the HELOC be settled or refinanced within 6 to 12 months of the owner’s passing. Always consult with a Probate Attorney to understand your state’s specific protections for heirs.

Probate Legacy Saver

Will your home get stuck in court? Use our Probate Legacy Saver to see how a HELOC balance affects the speed of your estate transfer and how to avoid the “Legal Limbo” that costs families thousands.

Frequently Asked Questions (FAQ)

No. Your children are not personally liable for your debts unless they co-signed the loan. The bank’s only “collateral” is the house itself. If the house is worth less than the debt (rare in today’s market), the bank usually has to take the loss.

If you die “Intestate” (without a will), the home goes through a longer probate process. The HELOC continues to accrue interest during this time, which “eats” the equity you intended to leave behind. Having a clear Beneficiary Plan is essential.

Yes. With a Reverse Mortgage (HECM), the heirs have up to 6 months (and sometimes up to a year) to decide whether to sell or walk away. It is a “non-recourse” loan, meaning the bank can never ask for more than the home is worth, even if the debt is higher.

A Living Trust can help the home bypass probate, which saves time. However, the Trust does not erase the HELOC lien. The Trust must still pay the bank before the house can be distributed to your heirs.

Check your most recent statement for the “Current Principal Balance.” Do not confuse this with your “Credit Limit.” Your legacy plan should be based on the actual balance you have drawn, plus a 10% buffer for future interest.

Explore Debt Relief Options (Secure your equity and protect your family’s inheritance today.)