You’ve done all the responsible planning. You’ve compared the options and secured a final expense policy to protect your loved ones.

But one question might still be in the back of your mind: “When the time comes, will this be a hassle for my family?”

It’s a critical question. You’re not buying this policy for yourself; you’re buying it so your family can grieve without financial stress. The last thing you want is for them to face a mountain of paperwork or a long, complicated claims process.

As your trusted guide, we’re here to show you just how simple and fast the payout process actually is.

Key Takeaways

- It’s a Simple 3-Step Process: Your beneficiary just needs to contact the insurer and provide the death certificate.

- It’s Fast: The payout is typically sent in a matter of days, not weeks or months.

- It’s 100% Tax-Free: The money your family receives is not considered income and is not taxed by the IRS.

- It’s Flexible Cash: The money is paid directly to your beneficiary to use for the funeral, final bills, or anything else—no restrictions.

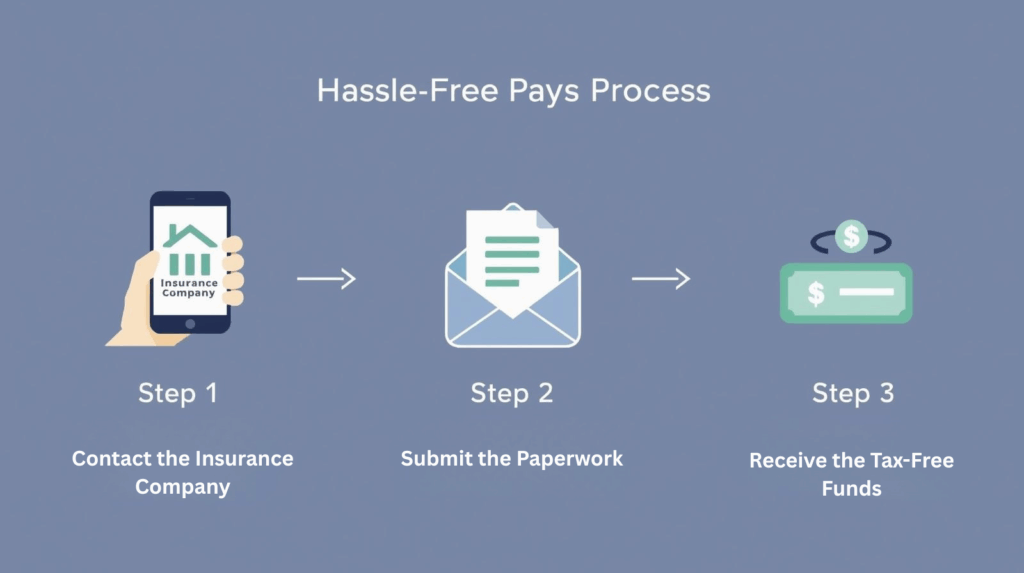

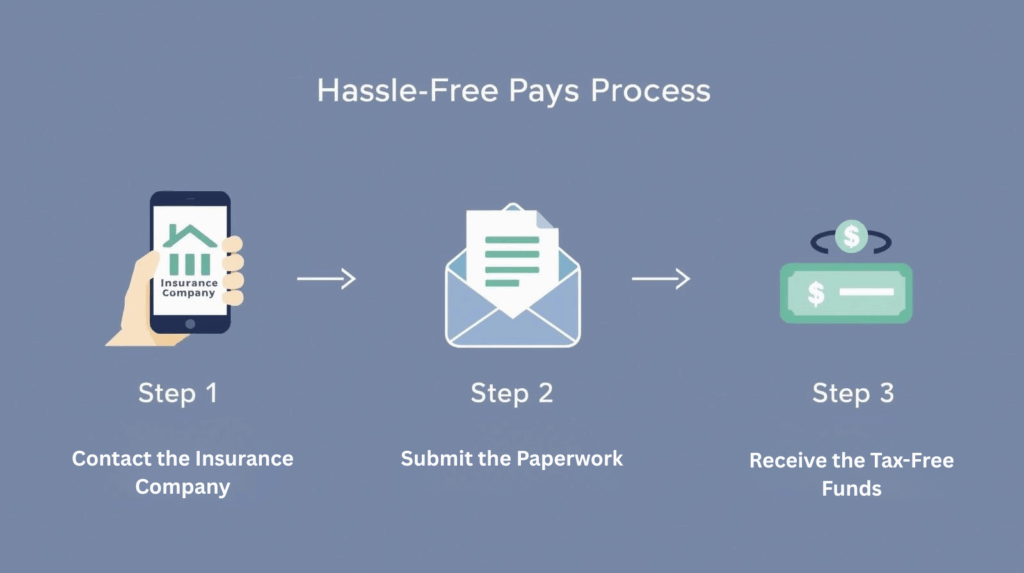

The 3-Step "Hassle-Free" Payout Process

Here is the entire process your beneficiary will follow. We’ve broken it down into a simple, visual guide.

- Contact the Insurance Company: Your beneficiary makes a phone call to the insurer’s claims department. They will need to provide your name, policy number, and the date of passing.

- Submit the Paperwork: The insurer provides a short “claims form.” Your beneficiary fills it out and sends it back with one critical document: a certified copy of the death certificate.

- Receive the Tax-Free Funds: Once the paperwork is received, the claim is processed (typically in 3-7 business days) and a check for the full benefit amount is mailed directly to your beneficiary.

Your "Peace of Mind" Checklist: 4 Things to Do Today

You can make this simple process even easier for your family. Take 10 minutes today to fill out this information and put it in a clearly labeled “Peace of Mind” folder. Tell your beneficiary where it is.

- [ ] 1. The Policy Details:

- Insurance Company Name: _____________

- Policy Number: _____________

- Claims Phone Number: _____________

- [ ] 2. Beneficiary Information:

- Primary Beneficiary: _____________

- Contingent (Backup) Beneficiary: _____________

- [ ] 3. A Copy of the Policy: Staple the main “declarations page” of your policy to the checklist.

- [ ] 4. A Note of Reassurance: Add a simple note reminding them you did this so they wouldn’t have to worry about money.

Why This is So Much Better Than a Bank Account

This is the most important “why” of all. Why not just leave $15,000 in a savings account?

When a person passes away, their bank accounts are immediately frozen.

Your family cannot access that money, even if their name is on the account. The bank must wait for a legal process called “probate,” which can take weeks or even months. But the funeral home needs to be paid now.

A life insurance policy bypasses probate entirely. The table below shows the critical difference.

|

Feature

|

Life Insurance Payout

|

Bank / Savings Account

|

|---|---|---|

|

Availability

|

Paid in days. (Bypasses probate)

|

Frozen. (Locked by probate for weeks/months)

|

|

Protection

|

Protected from creditors & medical bills.

|

Vulnerable to being seized for final debts.

|

|

Taxes

|

100% Tax-Free Payout.

|

Taxed. (Interest is taxed; part of the estate).

|

|

Result

|

Instant cash for your family.

|

A legal hassle for your family.

|

Beneficiary vs. Executor: Who is in Charge of What?

This is an expert-level tip that is critical to understand. The life insurance payout goes to the Beneficiary named on the policy, not to the Executor of the will.

- The Executor’s job is to settle the estate (probate, bank accounts, property). This is a long process.

- The Beneficiary’s job is to receive the insurance money. This is a fast, separate process.

This separation is why life insurance is so powerful. It bypasses the entire estate and gets money to your loved one (the Beneficiary) immediately.

Frequently Asked Questions (FAQ)

Once the insurer receives the correct paperwork (the completed claim form and the certified death certificate), it typically takes 3-7 business days to process the claim and mail the check.

The beneficiary keeps every extra penny, 100% tax-free. If you have a $15,000 policy and the funeral costs $10,000, your beneficiary has $5,000 left to cover travel, medical bills, or anything else.

This happens. If you believe a policy exists but can’t find it, you can use the free policy locator service from the National Association of Insurance Commissioners (NAIC) to search company records.

This is a smart question. You can name a “contingent beneficiary” (a backup) or even have the money paid to a trusted funeral home directly, but most people find it best to name their most responsible adult child as the primary beneficiary.

Your Final Act of Care

This policy isn’t just a piece of paper. It’s a plan. It’s the guarantee that your final act is one of care, not chaos. You are ensuring your family has the funds they need, exactly when they need them, with no hassle.

At Sagewise, we help seniors put this simple, loving plan in place every day.

Get a free, instant quote to see how affordable it is to give your family this final gift.